Choosing between a fixed or variable interest rate is one of the most important financial decisions property investors make and in today’s environment, it has become even more strategic. With interest rates having risen rapidly in recent years and now showing signs of stabilisation, investors are faced with a key question: should you lock in certainty or remain flexible?

The answer isn’t simply about which rate is lower today. It’s about understanding how rate cycles, cash flow, and long-term strategy all interact.

Understanding Fixed vs Variable Rates

A fixed interest rate locks in your repayments for a set period, providing certainty and protection from further rate increases. In contrast, a variable rate moves in line with market conditions, meaning your repayments can rise or fall over time.

In a rising rate environment, fixed rates can offer stability and peace of mind. However, once rates begin to stabilise or potentially fall, variable rates can provide greater flexibility and the opportunity to benefit from lower repayments.

The Current Rate Environment

Australia has moved through a period of aggressive rate increases aimed at controlling inflation. While rates remain elevated, the pace of increases has slowed, and markets are beginning to anticipate a period of stability.

This shift changes how investors should think about fixed versus variable decisions. Rather than reacting to past rate hikes, the focus should now be on what happens next in the cycle.

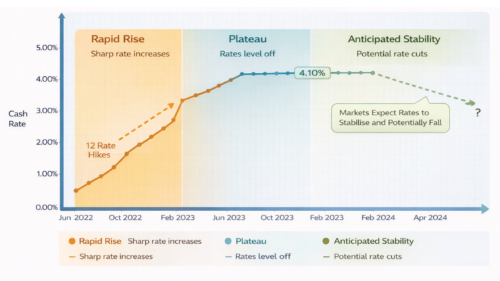

Australia’s Interest Rate Cycle: From Rapid Increases to Stabilisation

This graph illustrates the recent interest rate cycle in Australia, showing a period of rapid rate increases followed by a plateau. It highlights how rates are now stabilising, with markets beginning to anticipate a more steady environment. This shift is important for investors, as it signals a transition from tightening conditions toward a more predictable phase in the property and lending cycle.

Fixed Rates: Certainty in Uncertain Times

Fixed rates are often attractive during periods of volatility. They provide predictable repayments, which can be particularly valuable for investors managing multiple properties or tight cash flow.

Locking in a fixed rate can protect against further increases, allowing investors to plan with confidence. However, the trade-off is reduced flexibility. If rates fall, investors on fixed rates may not benefit unless they refinance, which can involve costs.

Variable Rates: Flexibility and Opportunity

Variable rates offer adaptability. As interest rates stabilise or decline, borrowers on variable rates can benefit from lower repayments without needing to refinance.

This flexibility also allows investors to make additional repayments, access offset accounts, or restructure loans more easily. In a stabilising or declining rate environment, this can become a significant advantage.

The Strategic Approach: It’s Not Either-Or

Many experienced investors don’t treat this as a binary decision. Instead, they use a combination of both.

Splitting loans between fixed and variable rates allows investors to:

- Maintain some certainty in repayments

- Retain flexibility to benefit from rate changes

- Balance risk across different market scenarios

This approach can provide a more resilient structure, particularly in uncertain or transitional rate environments.

Aligning Your Choice With Your Strategy

The right choice depends on your individual investment strategy. Investors focused on cash flow stability may lean toward fixed rates, while those prioritising flexibility and long-term growth may prefer variable rates.

It’s also important to consider factors such as portfolio size, risk tolerance, and future plans. There is no one-size-fits-all solution, only what best aligns with your broader investment goals.

Frequently Asked Questions (FAQ)

- Is it better to fix or stay variable right now?

It depends on your strategy and expectations. Fixed offers certainty, while variable offers flexibility. - Can I split my loan between fixed and variable?

Yes, many lenders allow loan splitting, which can balance risk and flexibility. - What happens if rates fall and I’m on a fixed rate?

You may not benefit from lower rates unless you refinance, which could involve break costs. - Are variable rates riskier?

They can be, as repayments may increase if rates rise. However, they also provide flexibility and potential savings if rates fall.

- How do I decide what’s right for me?

Consider your cash flow, risk tolerance, and long-term investment strategy rather than focusing only on current rates.

What This Means for Property Investors

In today’s environment, the decision between fixed and variable rates should be strategic, not reactive. Understanding where we are in the interest rate cycle can help investors make more informed choices.

At Citadel Agency, we help investors structure their portfolios to adapt to changing market conditions. If you’re deciding how to position your loans, you can connect with our team. You can also access more insights through our property investment guidance hub.