Despite one of the most aggressive interest rate tightening cycles in recent years, Australia’s property market has shown surprising resilience. Many expected a sharp downturn, yet prices in many regions have held firm and in some cases, even continued to rise. So why hasn’t the market crashed?

Understanding this comes down to looking beyond interest rates alone and examining the broader forces shaping supply, demand, and investor behaviour.

Interest Rates vs Property Prices: Not a Simple Relationship

While interest rates influence borrowing capacity and buyer sentiment, they don’t operate in isolation. Historically, property prices may slow or dip when rates rise, but they rarely collapse unless multiple negative factors occur at once.

This is because property markets are driven by a combination of lending conditions, population growth, housing supply, and employment levels, not just the cost of borrowing.

Strong Population Growth Supporting Demand

One of the biggest reasons the market has remained stable is strong population growth. Australia has seen a significant increase in migration, which directly fuels housing demand. Population growth has accelerated in recent years, placing additional pressure on already limited housing supply.

This surge in demand means that even when borrowing becomes more expensive, there are still enough buyers and renters in the market to support prices.

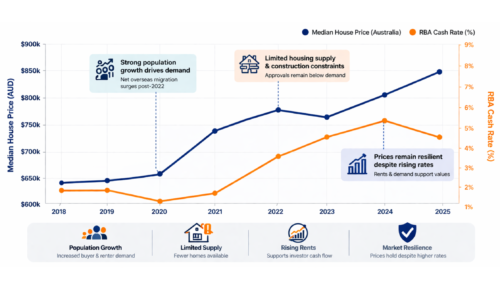

Property Market Resilience Amid Rising Interest Rates

This graph illustrates the relationship between interest rate increases (RBA cash rate) and property price movements in Australia over recent years. You’ll typically see that while interest rates rose sharply, property prices only experienced short-term slowdowns or minor declines before stabilising or recovering.

Limited Housing Supply

At the same time, housing supply has not kept pace with demand. Construction constraints, rising building costs, and labour shortages have slowed the delivery of new housing.

Supply shortages can sustain property prices even during periods of higher interest rates. When there are fewer properties available, competition remains strong among buyers.

Rental Market Pressure

Another key factor is the rental market. With fewer people able to buy due to higher rates, more people are renting, which increases demand for rental properties. This has pushed rents higher across many parts of Australia, helping investors maintain or even improve cash flow despite rising mortgage costs. According to insights from a Domain report on Australia’s rental shortage and rising rents, vacancy rates have fallen to extremely low levels while rental prices have reached record highs across major cities.

Higher rental income can offset increased interest expenses, reducing the likelihood of forced selling among investors.

Strong Employment and Household Resilience

The broader economy has also played a role. Australia has maintained relatively strong employment levels, which helps households continue servicing their mortgages even as repayments rise.

When people remain employed and income levels are stable, the risk of widespread mortgage defaults, a key driver of property crashes, remains low.

Lending Buffers and Tighter Regulations

Another often overlooked factor is how lending standards have changed. Australian borrowers are typically assessed at higher interest rate buffers, meaning they are already tested for their ability to repay loans even if rates rise.

This has created a more resilient borrower base compared to previous cycles. As a result, fewer

Frequently Asked Questions (FAQ)

- Why didn’t property prices crash when interest rates increased?

Because other factors like population growth, limited housing supply, and strong employment continued to support demand. - Do interest rates still affect property prices?

Yes, but they are only one factor. They influence borrowing capacity but don’t solely determine price movements. - Is it still a good time to invest during high interest rates?

It can be, especially if competition is lower and rental demand is strong. - What role does rental demand play?

High rental demand supports investor cash flow and reduces the likelihood of forced selling. - Will the property market crash in the future?

Markets can fluctuate, but a crash usually requires multiple negative conditions, not just rising interest rates.

What This Means for Investors

The key takeaway is that interest rates alone do not determine market outcomes. While they influence affordability and timing, other factors, particularly supply and demand, often play a more dominant role.

For investors, this reinforces the importance of taking a long-term view rather than reacting to short-term market conditions.

If you’re navigating today’s market, you can connect with our team to explore your options. You can also access more insights through our property investment guidance hub.