Property investment returns are shaped by more than rental yield and capital growth. Income tax, land tax, and capital gains tax (CGT) operate at different stages of ownership and collectively determine true net profitability.

If you’re trying to navigate these changes or make a smarter property decision, speaking with a property expert through a consultation can help you understand your options in today’s market.

Income Tax: The Annual Cash Flow Component

Income tax applies to net rental income after allowable deductions. These deductions may include interest expenses, property management fees, maintenance, depreciation, insurance, and council rates.

If expenses exceed rental income, the property may generate a tax-deductible loss. If income exceeds expenses, the surplus is taxed at the investor’s marginal rate.

The key consideration is that income tax directly affects liquidity. Even a positively geared property may produce lower-than-expected cash flow once marginal tax obligations are applied. Conversely, negatively geared properties may improve overall tax position but still require strong cash reserves.

Annual tax impact therefore shapes holding strategy and service ability planning.

Land Tax: The Recurring Holding Cost

Land tax is imposed annually by state governments based on the unimproved value of land holdings above a set threshold. Unlike income tax, it applies regardless of rental profitability.

As portfolios grow or land values appreciate, investors may cross threshold levels and face increasing land tax exposure. This can significantly reduce net yield in high-value metropolitan markets.

Land tax also compounds over time. Rising land values can increase annual tax obligations even if rental growth moderates, which makes long-term modelling essential.

Investors often underestimate land tax escalation when calculating projected returns.

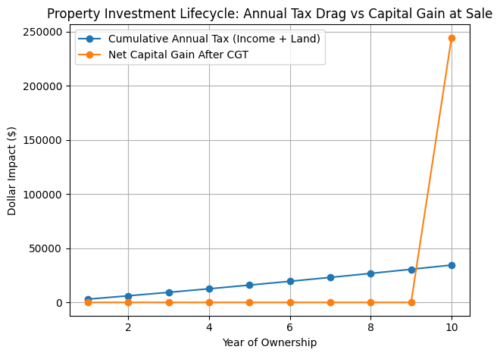

Graph: Annual Tax Costs Accumulate Gradually While Capital Gains Are Realized at Exit

This graph illustrates how income tax and land tax create a steady annual drag on cash flow over the holding period, while capital gains tax only impacts returns at the point of sale. Although recurring taxes reduce yearly profitability, long-term capital growth can significantly outweigh cumulative holding costs when the property is sold.

Capital Gains Tax (CGT): The Exit Adjustment

CGT applies when a property is sold and a capital gain is realised. The gain is calculated as the difference between sale proceeds and the cost base, which includes acquisition costs and eligible capital improvements.

For assets held longer than 12 months, individuals and trusts generally qualify for a 50% discount before applying marginal tax rates.

While CGT does not affect annual cash flow, it materially reduces final realised profit. Investors focusing solely on gross capital appreciation without modelling CGT may overestimate net proceeds.

The longer the holding period and the stronger the growth, the more relevant CGT planning becomes.

Understanding where the market is heading is essential, and working with experienced professionals can help you make more confident, data-driven decisions.

Conclusion

Property taxation is not a single event but a layered process that unfolds over time. Income tax shapes short-term cash flow, land tax influences holding viability, and CGT determines final realised returns.

Focusing on only one element can distort investment analysis. True profitability emerges from understanding how these tax components interact across the entire ownership lifecycle.

Strategic planning requires modelling annual obligations alongside exit implications, ensuring decisions are based on net outcomes rather than gross projections.

Frequently Asked Questions (FAQ)

- Do all property investors pay land tax? Land tax applies when land value exceeds state thresholds and varies by jurisdiction.

- Is CGT separate from income tax? CGT is assessed within the income tax framework but applies only when a CGT event occurs.

- Can rental losses reduce other income? In many cases, rental losses may offset other taxable income, subject to eligibility rules.

- Does land tax affect CGT calculations? Land tax does not directly alter CGT calculations but affects overall net returns.

- Which tax has the biggest impact? Impact depends on holding period, growth rate, land value, and marginal tax rate.

- Should investors prioritise CGT planning? CGT planning is important, but recurring tax obligations also significantly affect long-term returns.