Understanding how interest rate cycles and property cycles interact is one of the most important and often misunderstood aspects of property investing. While many assume that rising interest rates automatically lead to falling property prices, the reality is far more nuanced. Property markets move in cycles influenced by multiple factors, and interest rates are just one piece of a much larger puzzle.

What Are Interest Rate Cycles?

Interest rate cycles refer to the periods where central banks, such as the Reserve Bank of Australia, adjust rates to manage inflation and economic growth. Rates typically move through phases, rising during inflationary periods and falling during economic slowdowns.

When rates increase, borrowing becomes more expensive, which can reduce demand. When rates fall, borrowing becomes cheaper, encouraging spending and investment. However, these changes don’t impact the property market in isolation or immediately.

What Are Property Cycles?

Property cycles move through four key phases: growth, peak, decline, and recovery. These phases are driven by supply and demand, economic conditions, population growth, and investor sentiment.

Unlike interest rates, which can change quickly, property cycles tend to move more slowly. This lag is one of the key reasons why the relationship between interest rates and property prices isn’t always straightforward.

The Lag Effect Between Rates and Property

One of the most important concepts to understand is the lag effect. Changes in interest rates don’t instantly translate into changes in property prices.

When rates rise, it takes time for:

- Borrowers to feel the full impact

- Buyer sentiment to shift

- Supply and demand dynamics to adjust

This delay means property prices may continue rising even after interest rates begin increasing or stabilise before rates start falling.

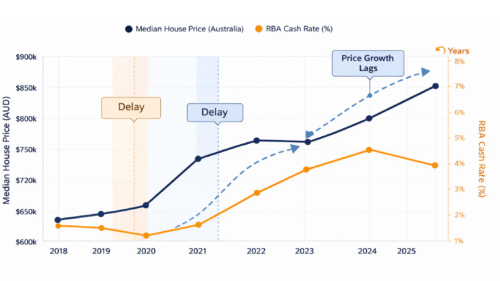

How Property Prices Respond Over Time to Interest Rate Changes

This graph illustrates the lag effect between interest rate movements and property price trends in Australia. While interest rates can rise or fall relatively quickly, property prices typically respond more gradually. The delay reflects how long it takes for higher borrowing costs to impact buyer behaviour, lending capacity, and overall market sentiment.

As shown, property prices may continue to grow even after interest rates begin rising, and may stabilise or recover before rates start to fall. This highlights that property markets are driven by longer-term fundamentals, with interest rates influencing timing rather than dictating immediate outcomes.

Why Rising Rates Don’t Always Mean Falling Prices

Higher interest rates can slow price growth, but they don’t automatically cause declines. This is because other factors, such as population growth, housing shortages, and employment levels can continue supporting demand.

In many cases, rising rates simply reduce the speed of growth, rather than reversing it. Property markets are resilient because they are driven by long-term fundamentals, not just short-term financial conditions.

When Falling Rates Accelerate Property Growth

Lower interest rates tend to have a stronger and more immediate impact on property markets. As borrowing becomes more affordable, more buyers enter the market, increasing competition.

This often leads to:

- Faster price growth

- Increased investor activity

- Higher transaction volumes

However, even here, the effect is amplified when combined with strong economic conditions and limited housing supply.

The Role of Supply and Demand

Interest rates influence demand, but supply plays an equally important role. When housing supply is limited, prices can remain stable or even rise despite higher interest rates.

This imbalance is a key reason why Australia’s property market has remained resilient in recent years. Even as borrowing costs increased, strong demand and limited supply continued to support prices.

Investor Strategy Across Cycles

Successful investors don’t react to interest rates alone, they understand where the market sits within the broader property cycle.

During rising rate periods, experienced investors often:

- Focus on long-term growth rather than short-term conditions

- Target areas with strong fundamentals

- Take advantage of reduced competition

During falling rate periods, they position themselves early to benefit from increased demand and price growth.

Frequently Asked Questions (FAQ)

- Do property prices always fall when interest rates rise?

No. Rising interest rates often slow price growth, but other factors like demand and supply can keep prices stable or rising. - Why is there a lag between interest rates and property prices?

Because it takes time for borrowing costs, buyer behaviour, and market conditions to adjust. - When is the best time to invest in the property cycle?

Opportunities can exist at all stages, but many investors target early growth or recovery phases. - Do lower interest rates guarantee property price increases?

Not always, but they typically increase demand and can accelerate growth when combined with strong fundamentals. - How should investors respond to interest rate changes?

By focusing on long-term strategy, cash flow management, and market fundamentals rather than short-term movements.

What This Means for Investors Today

The key takeaway is that interest rates and property cycles are connected, but not in a simple cause-and-effect way. Interest rates influence borrowing and sentiment, while property cycles are shaped by broader economic and demographic forces.

Understanding this interaction allows investors to make more informed decisions, avoid reacting emotionally to rate changes, and focus on long-term outcomes.

At Citadel Agency, we help investors interpret market cycles and align their strategy with the right opportunities. If you want to better understand your position in the current cycle, you can connect with our team. You can also access more insights through our property investment guidance hub.