Australia’s property market is influenced by more than just interest rates. Lending standards also play a major role in determining how much buyers can borrow and how confident they feel entering the market. Even when demand remains strong, tighter credit conditions can affect the pace of activity and shift buyer behaviour.

In 2026, lending standards remain a key factor shaping buyer activity. Banks continue to assess borrowers using serviceability buffers, detailed expense reviews, and stricter documentation requirements. These measures are designed to reduce risk, but they can also limit how much buyers are able to borrow.

For investors and owner-occupiers alike, understanding how lending standards affect market dynamics is essential. While tighter credit can slow activity, it does not necessarily lead to falling prices when supply remains constrained and demand fundamentals stay strong.

What Are Lending Standards?

Lending standards are the rules and assessment criteria lenders use to determine whether a borrower qualifies for a loan. These include income verification, debt-to-income ratios, credit history, living expenses, and serviceability buffers applied above the actual interest rate.

In Australia, lenders are required to assess whether borrowers can still afford repayments if interest rates rise further. This conservative approach helps reduce the risk of financial stress and loan defaults.

Although these standards improve financial stability, they can also reduce borrowing capacity, especially when rates are already elevated. This directly affects how much buyers can spend and which markets they can target.

Borrowing Capacity Declines

One of the most immediate effects of tighter lending standards is reduced borrowing capacity. Even if a buyer’s income remains unchanged, stricter assessment rates can lower the amount they are approved to borrow.

This often leads buyers to adjust their expectations by targeting more affordable suburbs, smaller properties, or lower price brackets. Some may delay purchasing altogether while they improve their financial position.

Buyer Demand Shifts Rather Than Disappears

Reduced borrowing power does not mean demand vanishes. Instead, it tends to shift toward more affordable markets and property types where buyers can still secure finance.

This adjustment is one reason affordable suburbs often outperform premium segments during periods of tighter credit. Buyers remain active, but they become more selective and practical in their purchasing decisions.

Approval Times and Documentation Matter

Tighter lending standards can also increase the time and effort required to obtain finance. Lenders may request additional documentation, scrutinise spending patterns more closely, and take longer to assess applications.

This can affect buyer confidence, especially in competitive markets where speed matters. Buyers who are well prepared with up-to-date financial records and pre-approval are often better positioned to act quickly.

For investors, maintaining organised financials and working with experienced finance professionals can reduce delays and improve approval outcomes.

Property Prices Can Remain Resilient

Even when lending standards restrict borrowing capacity, prices do not automatically decline. Property values are still influenced by broader factors such as population growth, housing supply, employment, and rental demand.

If supply remains limited and demand continues to outpace available stock, prices may stabilise or keep rising despite tighter credit conditions.

This demonstrates why lending standards are only one part of the market equation. Their impact depends on how they interact with other economic and structural factors.

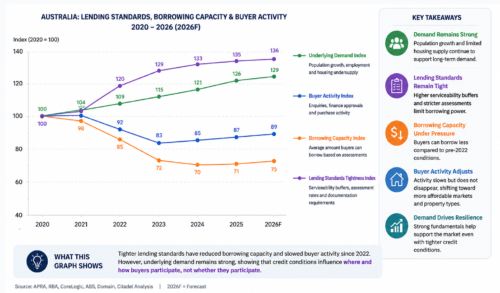

Lending Standards, Borrowing Capacity & Buyer Activity 2020-2026

This graph illustrates how tighter lending standards can reduce borrowing capacity and slow buyer activity, while overall demand remains supported by strong market fundamentals.

It highlights that credit conditions influence where and how buyers participate rather than eliminating demand altogether.

Frequently Asked Questions (FAQ)

- What are lending standards?

They are the criteria banks use to assess whether borrowers can safely service a loan. - Do tighter lending standards reduce property prices?

Not necessarily. Prices depend on supply and demand, not borrowing capacity alone. - How do tighter standards affect buyers?

They reduce borrowing capacity and may shift demand toward more affordable properties. - Why are serviceability buffers important?

They test whether borrowers can afford repayments if interest rates rise further. - Can investors still buy successfully?

Yes. Many adapt by targeting high-demand, affordable markets and improving their financial preparation.

What This Means for Property Investors

Tighter lending standards are reshaping buyer behaviour, but they are not stopping investment activity. Buyers are adapting by focusing on affordability, preparing documentation more carefully, and targeting markets where finance remains achievable.

For investors, this creates opportunities in segments with strong rental demand and accessible price points. Understanding how lenders assess applications can also improve strategic decision-making.

At Citadel Agency, we help investors identify properties that balance cash flow, growth potential, and long-term strategic value. Explore our property strategy resources for more expert insights.

If you’d like tailored guidance based on your investment goals, contact our team for personalized support.