Capital Gains Tax has long been central to Australia’s property investment landscape. Whenever policy reform is discussed, headlines often suggest dramatic consequences for investors and the broader housing market. Proposals to reduce the CGT discount, adjust negative gearing rules, or tighten exemptions tend to generate strong reactions from investors, industry bodies, and policymakers alike.

The real question is whether potential CGT changes would materially harm property investors or whether the impact is frequently overstated. To answer that properly, it is necessary to understand how CGT currently operates, what reforms have been proposed historically, how markets have reacted to past tax adjustments, and how investor behaviour adapts over time.

This analysis examines the issue in a balanced, evidence-based manner, supported by official sources and economic commentary.

Understanding the Current CGT Framework

Capital Gains Tax in Australia is governed by federal legislation and administered by the Australian Taxation Office. It is not a standalone tax but forms part of an individual’s income tax. When an investment property is sold at a profit, the gain is included in assessable income in the financial year in which the contract is signed.

The Australian Taxation Office explains that individuals and trusts may apply a 50 per cent CGT discount if the asset has been held for more than 12 months, as detailed on theATO CGT discount guidance. This discount significantly reduces the taxable portion of long-term capital gains and is widely regarded as a key driver of investment property holding strategies.

Because gains are taxed at marginal rates after the discount is applied, the effective tax rate for many investors is substantially lower than their headline marginal income tax rate.

What CGT Changes Have Been Proposed?

Debate around CGT reform is not new. Over recent years, several policy discussions have included reducing the CGT discount from 50 per cent to 25 per cent or restructuring negative gearing arrangements. These discussions have often appeared in federal election policy platforms and budget commentary.

The Parliament of Australia provides access to legislative proposals and historical bills through its official website, including taxation reform debates, which can be reviewed via the Parliament of Australia bills archive.

Although no major structural change to the CGT discount has been enacted in recent years, the recurring debate contributes to investor uncertainty. However, uncertainty alone does not necessarily translate into long-term market damage.

Would Reducing the CGT Discount Significantly Lower Investor Returns?

To understand the practical impact, consider a simplified scenario. Assume a property generates a $200,000 capital gain after being held for more than 12 months.

Under the current 50 per cent discount system, only $100,000 is taxable. If the investor’s marginal tax rate is 37 per cent, the tax payable would be $37,000.

If the discount were reduced to 25 per cent, $150,000 would become taxable. At a 37 per cent marginal rate, tax payable would increase to $55,500.

The difference in tax is $18,500. While meaningful, it must be assessed in the broader context of total investment performance, rental yield, depreciation benefits, and capital growth over time.

In most long-term investment scenarios, capital growth is influenced more heavily by supply constraints, population growth, infrastructure development, and credit conditions than by marginal tax rate adjustments alone.

Historical Evidence: Do Tax Changes Crash Property Markets?

International and domestic evidence suggests that property markets are complex systems influenced by multiple variables. Historically, Australian property markets have demonstrated resilience despite policy shifts, including changes to lending standards and investor credit restrictions. While short-term investor activity may fluctuate in response to tax uncertainty, long-term structural demand tends to stabilise the market.

This suggests that while CGT reform may affect investor behaviour at the margin, broader macroeconomic forces play a more dominant role in price outcomes.

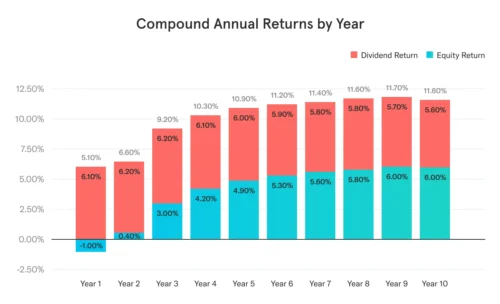

Graph: How Long-Term Capital Growth Reduces the Relative Impact of CGT

This chart shows 10 years of compound annual returns, split between dividend income and equity growth. Early returns are modest, but equity growth strengthens over time and becomes the main driver of total performance, while dividends remain steady. It highlights how long-term investing benefits from compounding and growing capital appreciation.

Is the Fear Overstated?

Public debate often amplifies worst-case scenarios. While reduced CGT concessions would decrease after-tax returns, the effect may be proportionally smaller than media narratives suggest.

Property remains influenced by population growth, migration levels, land scarcity, infrastructure spending, and interest rates. The Reserve Bank of Australia consistently emphasises these drivers in its housing market commentary.

Investors who adopt a long-term strategy, diversify appropriately, and plan for tax liabilities may find that CGT reform represents a manageable adjustment rather than a market-breaking event.

Frequently Asked Questions (FAQ)

1. Would a reduction in the CGT discount make property investing unprofitable?

Not necessarily. It would increase tax payable on gains, but profitability depends on total return, not just tax treatment.

2. Has Australia removed the CGT discount before?

The current discount system has operated since 1999. Any structural change would require federal legislation.

3. Would CGT changes affect existing properties?

Policy proposals typically specify commencement dates. Historically, reforms may apply prospectively, though legislative detail matters.

4. Do companies receive the CGT discount?

No. Companies are taxed on capital gains without the 50 per cent discount.

5. Are CGT changes likely to cause property prices to fall?

Research suggests broader economic factors such as interest rates and supply constraints play a larger role in price movements.

Should investors delay selling due to reform speculation?

Tax decisions should be based on confirmed legislation and individual financial planning rather than speculation.

Conclusion

Capital Gains Tax reform remains a politically sensitive topic in Australia. While reducing the CGT discount would increase tax payable on investment property gains, the magnitude of impact should be evaluated within the broader context of overall returns, economic conditions, and investor adaptability.

Historical evidence and economic research suggest that property markets are influenced more strongly by structural supply-demand dynamics and monetary policy than by marginal tax adjustments alone.

For investors, the most effective response is not alarm but preparation. Understanding tax mechanics, modelling potential scenarios, and seeking professional advice ensures that any future CGT change is incorporated into strategic decision-making rather than feared as an existential threat.

EXTERNAL LINKS: