After the sharp rental surge of 2022 and 2023, many analysts anticipated a cooling phase. Interest rates had risen, affordability pressures intensified, and household budgets were tightening. The prevailing expectation was that rental growth would decelerate materially.

Yet across much of Australia, rents have remained resilient and in several markets, continued rising. This raises an important question: why hasn’t rental growth slowed the way many predicted?

Migration Has Remained Elevated

One of the strongest drivers of rental demand has been net overseas migration. While forecasts suggested moderation, migration levels have remained comparatively strong, particularly in major metropolitan areas.

When population growth outpaces housing supply, rental demand persists regardless of interest rate settings. The absorption capacity of rental markets has therefore remained under sustained pressure.

Housing Completions Have Lagged Demand

Even as borrowing costs increased, dwelling completions did not accelerate sufficiently to rebalance supply. Construction delays, insolvencies within the building sector, and labour constraints limited new stock.

Without meaningful supply expansion, rental markets remained structurally tight. Slower construction activity reinforced upward pricing pressure despite affordability concerns.

Vacancy Rates Remain Below Long-Term Norms

Vacancy rates act as a leading indicator for rental direction. Although modest increases have appeared in selected regions, national vacancy levels remain historically low.

Tight vacancy conditions limit tenant choice and sustain competition. As long as vacancy remains constrained, broad-based rental declines are unlikely.

Higher Interest Rates Did Not Reduce Demand

Higher interest rates were expected to reduce investor participation and dampen rental growth. Instead, rate increases affected both landlords and aspiring homeowners.

Some prospective buyers delayed purchasing due to borrowing constraints, remaining in the rental pool longer. This extended rental demand even as ownership affordability weakened.

The net effect was continued pressure on rental markets rather than relief.

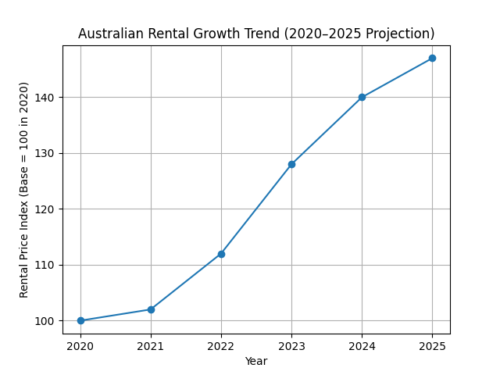

Graph: Rental Growth Remains Elevated Despite Expectations of a Slowdown

This chart shows the steady rise in rental prices from 2020 to 2024, followed by a projected moderation in 2025. While growth is beginning to ease, the data suggests rental markets remain structurally tight rather than entering a significant decline.

Table: Why Rental Growth Remained Resilient

|

Factor |

Expected Impact |

Actual Outcome |

|

Higher Interest Rates |

Reduced rental demand |

Delayed homeownership, sustained demand |

|

Wage Pressure |

Rental resistance |

Gradual affordability strain, not collapse |

|

Supply Pipeline |

Increased availability |

Construction lagged demand |

|

Migration |

Moderation expected |

Elevated inflows continued |

|

Vacancy Rates |

Normalisation |

Remained historically low |

This divergence between expectation and outcome explains why rental growth has not slowed as anticipated.

Are We Seeing the Beginning of Moderation?

While rental growth has remained firm, early signs of moderation are emerging in some regions. Vacancy rates are edging slightly higher and rental increases are occurring at a slower pace than peak growth periods.

This suggests not a reversal, but a transition from rapid acceleration to controlled expansion.

Structural supply constraints remain unresolved, limiting the likelihood of widespread rental declines in the near term.

Frequently Asked Questions (FAQ)

- Why didn’t higher interest rates reduce rents?

Higher rates delayed home purchases for many households, keeping them in the rental market longer.

- Are vacancy rates rising?

They have increased slightly in some areas but remain historically tight overall.

- Could rents still fall?

A sustained increase in supply or sharp demand contraction would be required for broad declines.

- Is migration still affecting rents?

Yes. Elevated population growth continues to support rental demand in major cities.

- Is rental growth slowing at all?

Growth appears to be moderating from peak acceleration, but not reversing nationally.

- What should investors watch next?

Vacancy rate trends, housing completion data, and migration policy changes will be key indicators.

Conclusion

Rental markets were widely expected to cool under the weight of rising interest rates and affordability strain. However, structural forces particularly migration levels and limited supply have maintained tight market conditions.

The anticipated slowdown has been softer than predicted because demand has remained elevated while supply has not expanded sufficiently.

While growth rates may ease, the underlying imbalance between rental demand and available housing stock suggests that meaningful downward pressure remains unlikely in the immediate term.

For investors, this reinforces the importance of monitoring supply trends and vacancy shifts rather than assuming interest rates alone dictate rental performance.

EXTERNAL LINK:

- Australia’s migration boom: where are our new migrants coming from?

- State of Housing Demand

- Rental vacancy rates sharply retreat to near record lows

- Why higher interest rates may not cool inflation – or home prices