Rental increases are often attributed to interest rates or landlord decisions. In reality, the most consistent drivers of rent movements are structural particularly vacancy rates and migration trends.

Across Australia, the sharp rise in rents over recent years has closely aligned with historically low vacancy levels and elevated population growth. Understanding how these forces interact provides clearer insight into why rents move and whether future increases are likely to persist.

This article examines the structural mechanisms behind rental growth and why vacancy and migration data matter more than short-term headlines.

Vacancy Rates: The Immediate Pressure Indicator

Vacancy rates measure the proportion of rental properties that are unoccupied at a given time. When vacancy rates fall below long-term averages, competition for available dwellings intensifies.

In tight markets typically below 2% vacancy tenants have fewer options, and landlords retain greater pricing leverage. Even modest increases in demand can result in significant rent adjustments when supply is constrained.

Low vacancy does not cause rents to rise independently; it reflects a supply-demand imbalance that enables rental growth.

To understand the magnitude of this relationship, recent Australian data shows vacancy rates falling to historically low levels, often below 1.5% nationally, well under the commonly accepted equilibrium range of 2.5%–3%. At these levels, tenants face significantly reduced bargaining power, while landlords experience minimal leasing risk. This imbalance creates conditions where even small increases in demand translate into disproportionately large rental price adjustments, particularly in capital cities where supply constraints are most acute.

Migration: The Demand Accelerator

Net overseas migration directly increases rental demand, particularly in capital cities where new arrivals tend to settle. When migration inflows exceed new housing completions, rental markets absorb immediate pressure. Unlike owner-occupiers, new migrants typically enter the rental market first, placing short-term strain on available stock.

Elevated migration therefore acts as a demand accelerator in already tight markets. This effect has been particularly evident following the post-pandemic reopening period, where net overseas migration surged above 400,000 annually. Unlike long-term residents, new arrivals overwhelmingly enter the rental market before transitioning to homeownership, creating immediate demand pressure. This front-loaded demand effect means that migration shocks impact rental markets far more rapidly than broader population growth alone would suggest.

Supply Pipeline and Construction Lag

Even when policymakers aim to increase housing supply, construction timelines limit immediate response. Planning approvals, labour shortages, and financing constraints can delay new completions.

If new housing supply lags behind household formation, vacancy rates remain compressed. Without meaningful supply expansion, rent pressure persists even when economic conditions soften. This lag effect explains why rental markets do not rebalance quickly.

Recent construction data reinforces this structural delay. Despite policy commitments to increase housing supply, dwelling approvals and completions have remained below required levels to meet population growth. Factors such as rising construction costs, builder insolvencies, and labour shortages have further constrained delivery timelines. As a result, even when demand begins to stabilise, insufficient new supply prolongs rental market tightness.

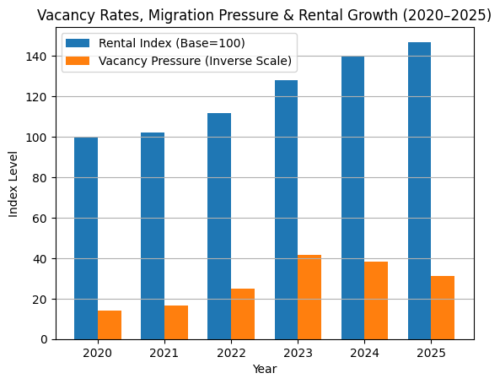

Graph: Tight Vacancies Continue to Drive Upward Rental Pressure

This chart highlights the inverse relationship between vacancy rates and rental growth from 2020 to 2025. As vacancy levels tightened, rental prices accelerated. Even with a slight projected easing in vacancy rates, rental pressure remains elevated, helping explain why rent growth has stayed resilient rather than declining.

Table: Core Drivers of Rent Increases

|

Driver |

Mechanism |

Rental Impact |

|

Low Vacancy Rates |

Limited rental availability |

Upward pricing pressure |

|

Strong Migration |

Increased household formation |

Higher rental demand |

|

Slow Construction |

Supply lag |

Sustained market tightness |

|

Delayed Homeownership |

Buyers remain renters |

Demand persistence |

|

Wage Growth |

Sets affordability ceiling |

Moderates future increases |

This combination of forces explains why rents have remained resilient despite expectations of slowdown.

What is particularly important is that these drivers do not operate independently. Instead, they reinforce one another. For example, strong migration increases household formation, which tightens vacancy rates, while construction delays prevent supply from responding. This interconnected dynamic creates a compounding effect, making rental markets more sensitive to shocks and slower to stabilise.

Why Interest Rates Alone Don’t Explain Rent Growth

Interest rates influence investor borrowing costs, but rental pricing ultimately depends on market balance. Even in high-rate environments, rents can rise if supply remains tight and demand remains elevated.

Conversely, rents can stabilize in low-rate environments if vacancy rates rise significantly. Structural imbalance, not monetary policy alone, is the primary driver.

While interest rates influence investor behaviour and borrowing capacity, their effect on rents is indirect. In some cases, higher interest rates can even reduce new housing supply by discouraging development, further tightening rental markets. This highlights why relying solely on monetary policy to address rental affordability is insufficient without parallel supply-side solutions.

Are Vacancy Rates Beginning to Ease?

Modest increases in vacancy rates have appeared in selected markets. If this trend continues and supply expands, rental growth may moderate.

However, until vacancy levels return to long-term equilibrium, upward pressure is likely to persist. The path of migration policy and housing completions will largely determine the next phase of rental movement.

Early indicators suggest that while vacancy rates have edged higher in some regions, they remain well below long-term averages. This suggests the market is transitioning from extreme tightness to moderate constraint rather than moving into surplus. As a result, rental growth may slow, but a sustained decline in rents would likely require a significant and prolonged increase in housing supply relative to demand.

Frequently Asked Questions (FAQ)

- Why are vacancy rates important? Low vacancy rates signal limited rental availability, increasing competition and supporting rent growth.

- Does migration directly increase rents? Yes. New arrivals typically enter the rental market first, increasing short-term demand.

- Can rents rise even if interest rates are high? Yes. Supply-demand imbalance can sustain rent increases regardless of borrowing costs.

- What would cause rents to stabilise? A sustained rise in vacancy rates driven by increased housing supply or reduced demand.

- Are vacancy rates rising now? Some markets show modest increases, but levels remain relatively tight overall.

- What should investors monitor next? Housing completions, migration trends, and vacancy data provide early indicators of rental direction.

Conclusion

Vacancy rates and migration patterns provide the clearest lens through which to understand rent increases. Tight supply conditions combined with elevated population growth have created sustained demand pressure across major markets.

While rental growth may moderate as vacancy rates gradually rise, structural imbalances remain evident. Meaningful relief requires sustained increases in housing supply relative to household formation.

For investors and policymakers alike, monitoring vacancy and migration trends is essential to anticipating future rental dynamics.

EXTERNAL LINK:

- National Vacancy Rates Fall to 1.2% in July — Rental Squeeze Intensifies

- The Migration Accelerator: Labor Mobility, Housing, and Demand

- Why higher interest rates aren’t to blame for the rental crisis

- Are High Interest Rates to Blame for the Rental Crisis?

- Rental markets ease slightly, but pressure remains as vacancies stay below long-term norms