Rents across Australia have risen sharply over the past several years, driven by tight vacancy rates, elevated migration, and constrained housing supply. While growth has begun to moderate in some areas, meaningful and sustained rent declines remain rare.

For rents to genuinely fall, not merely slow, structural conditions would need to shift significantly. Rental markets respond to imbalances in supply and demand. Without correcting those imbalances, downward pressure remains limited.

This article examines what would realistically need to change for rental prices to decline in a sustained and measurable way.

A Sustained Rise in Vacancy Rates

The most immediate trigger for falling rents is a sustained increase in vacancy rates. When available rental stock expands meaningfully relative to demand, competition shifts from tenants to landlords.

Historically, vacancy rates above approximately 3% have reduced upward rental pressure and in some cases contributed to price declines. For rents to fall nationally, vacancy rates would need to move well above tight-market thresholds and remain elevated for a sustained period.

Short-term fluctuations are not sufficient; structural loosening is required. A useful nuance here is that vacancy rates should be treated as a market signal rather than a universal mechanical threshold. Recent AHURI research notes that vacancy-rate measures in Australia are not fully standardised and can vary by methodology and location, which means a “balanced” market is not identical across every city. Even so, the broader principle still holds: when vacancies remain exceptionally low, tenants have fewer options, landlords face less competition, and rents tend to stay elevated. That makes a sustained lift in available rental stock more important than a brief seasonal rise in listings.

Accelerated Housing Supply

For vacancy rates to rise, housing completions must outpace household formation. This requires sustained construction growth rather than short-term policy announcements.

Planning approvals, labour availability, material costs, and developer financing conditions all influence supply pipelines. Without a meaningful expansion in completed dwellings, rental stock remains constrained.

The supply challenge is not just about building more dwellings in gross terms, but about whether growth in usable housing is actually keeping pace with household formation. Between the 2016 and 2021 Censuses, Australia added nearly one million new households, while dwelling growth lagged that pace once unoccupied homes are taken into account. That distinction matters because properties that are vacant, held as second homes, or otherwise unavailable to the long-term rental market do not relieve pressure for ordinary tenants. In practical terms, rents are unlikely to fall materially unless completions consistently outpace the growth in households competing for housing

A Meaningful Reduction in Migration

Migration is a major contributor to rental demand, particularly in capital cities. A sustained decline in net overseas migration would reduce short-term pressure on the rental market.

However, migration policy interacts with labour market needs and economic growth objectives. A sharp reduction may not align with broader economic priorities.

For rents to fall, demand growth would need to slow materially relative to housing supply.

It is also important not to frame migration as a stand-alone explanation for rental stress. Grattan Institute analysis argues that the sharper issue is the mismatch between rapid population growth and the capacity of the housing system to respond, especially because relatively few recent migrants work in residential construction. In other words, stronger migration increases housing demand more quickly than it expands the workforce needed to build additional homes. That is why rental pressure can persist even when migration normalises somewhat: unless supply responsiveness improves, the underlying imbalance remains.

Economic Contraction or Employment Weakness

Periods of economic contraction can reduce rental demand through slower household formation, increased consolidation of living arrangements, or outward migration from high-cost areas.

However, economic downturns also carry broader risks. While weaker demand may reduce rents, it typically coincides with wider financial strain across households and investors.

Rental declines linked to economic contraction are not generally considered healthy corrections.

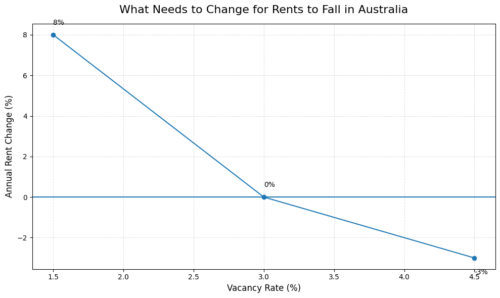

Graph: Rising Vacancy Levels Are the Key Trigger for Rental Declines

This graph illustrates the relationship between vacancy rates and annual rent changes. When vacancy levels remain tight, rents tend to rise. As vacancy approaches balanced conditions around 3%, growth stabilises. Sustained vacancy rates above 4% are typically required before meaningful rental declines occur, highlighting the structural shift needed for rents to fall in Australia.

Table: What Would Shift Rental Direction

|

Structural Change |

Market Effect | Likely Rental Outcome |

|

Vacancy Above 3% |

Increased tenant choice |

Stabilisation or decline |

|

Large-Scale Housing Completions |

Expanded rental stock |

Downward pressure |

|

Migration Slowdown |

Reduced new demand |

Moderation |

|

Economic Slowdown |

Lower household formation |

Potential declines |

|

Policy Reform (Supply-Focused) |

Faster approvals & delivery |

Gradual easing |

The table highlights that no single factor alone is sufficient; multiple drivers must align.

Why Rents Haven’t Fallen Yet

Although affordability pressure has increased, structural supply constraints remain evident. Construction pipelines have not expanded sufficiently to rebalance demand, and migration has remained elevated relative to dwelling completions.

There is some evidence that parts of the market are no longer accelerating at the same pace, but that should not be confused with genuine relief. Conditions in some cities are showing signs of stabilisation, while stressing that pressures remain severe and that in many cases renters may simply have reached their financial limit. That distinction strengthens your point: rents can stop rising as quickly because households are overstretched, yet still remain too high to describe the market as healthy or affordable

Even modest easing in vacancy rates has not yet reached levels consistent with broad-based rent declines.

Moderation is occurring in some regions, but a national reversal requires stronger structural change.

Conclusion

Rental prices do not fall simply because affordability tightens or interest rates rise. Sustained declines require a clear shift in structural market balance, typically through rising vacancy rates driven by expanded housing supply or reduced demand.

While moderation is emerging in select markets, the broader national picture still reflects constrained supply relative to household formation.

Until housing completions meaningfully exceed demand growth, widespread rent declines remain improbable.

For investors, monitoring vacancy trends and supply pipelines is more informative than focusing solely on monetary policy. For policymakers, meaningful rental relief depends primarily on sustained housing delivery rather than temporary intervention.

Frequently Asked Questions (FAQ)

- What vacancy rate level typically causes rents to fall? Vacancy rates above approximately 3–4% sustained over time can create downward rental pressure.

- Can rents fall without new housing supply? Significant demand reduction could contribute, but supply expansion is the most direct mechanism/

- Would lower interest rates reduce rents? Lower rates may increase demand by enabling more buyers, potentially reducing rental pressure indirectly.

- Is Australia currently oversupplied with rental housing? No. Most markets remain relatively tight.

- Could policy changes alone reduce rents? Policy can influence supply and demand, but structural delivery of housing is critical.

- Are rent declines likely in the near term? Based on current structural conditions, moderation is more likely than broad-based declines.

EXTERNAL LINKS:

- News Australian rental vacancies edge higher but supply stays critically tight Australian rental vacancies edge higher but supply stays critically tight

- Demystifying the rental vacancy rate measure: a critical review and policy implications

- Why is net overseas migration plummeting?

- Why does Australia have a rental crisis, and what can be done about it?

- Unemployment rate hides insidious labour market problems that are decreasing productivity

- How migration could help fix the housing crisis

- Rental Affordability Index 2025: Signs of stabilisation, but pressures remain high

- Rental market growth stalls in some capital cities as household budgets stretched to limit