If you’re serious about property investing, you can’t afford to skip investment property holding costs. Many investors focus on the purchase price and rental income, but the real measure of success lies in how much it costs you to hold the property over time. In this guide, you’ll learn how to calculate cash flow and holding costs in just five minutes using a simple step-by-step method designed for Australian investors. The thesis is simple: when you understand and model your holding costs upfront, you can make smarter, more confident investment decisions.

What Are Holding Costs and Why They Matter

When you buy an investment property, the purchase price is only the beginning. Holding costs, sometimes called ownership costs, refer to all the expenses involved in keeping the property tenanted or ready for rent. These typically include:

- Mortgage interest

- Council and water rates

- Land tax

- Insurance

- Strata or owners’ corporation fees

- Property management fees

- Maintenance and vacancy buffers

In Australia, many investors underestimate these expenses and end up with smaller profits than expected. As Realestate.com.au explains, the monthly cost of owning an investment property often includes much more than just loan repayments. By fully accounting for holding costs, you can budget accurately, select properties that truly align with your goals, and avoid unexpected cash flow shocks.

How to Calculate Investment Property Cash Flow in 5 Minutes

Here’s a quick and practical method for calculating your investment property’s cash flow and holding costs in under five minutes. You can easily create this worksheet in Excel or Google Sheets or use an online calculator such as The Property Forge’s Investment Calculator Australia.

Step 1: Estimate annual rental income

- Multiply weekly rent by 52 (for example, $550 × 52 = $28,600).

- Adjust for vacancy (e.g., assume 96% occupancy → $28,600 × 0.96 = $27,456).

Step 2: List all annual holding costs

- Mortgage interest (use your current interest rate and loan balance).

- Council, water, and land tax charges.

- Strata or owners’ corporation fees if applicable.

- Insurance (building and landlord).

- Property management fees, usually 6–8% of rent collected.

- Maintenance and repairs buffer, generally 5–10% of annual rent.

Step 3: Calculate net annual cash flow

Subtract total holding costs from your net rental income.

If the result is positive, you have positive cash flow. If it’s negative, you’re funding the shortfall yourself.

Step 4: Check break-even growth

If your property is negatively geared, calculate the minimum capital growth you need each year to offset the loss. For example, if your annual shortfall is $4,000 on a $500,000 property, you’ll need around 0.8% growth to break even before tax.

Step 5: Use or build a calculator

Free tools like The Property Forge Investment Calculator make this process simple. Just input your numbers to see your property’s cash flow snapshot in seconds.

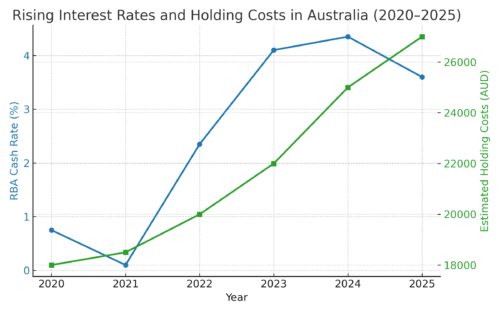

Recent data shows that nearly 65% of Australian investors reported negative cash flow in 2024, up from 57% in 2023 (Realestate.com.au). This highlights why understanding your numbers is critical before buying.

Common Pitfalls and Questions When Calculating Holding Costs

Even with the best intentions, investors often make mistakes when estimating holding costs. Here are the most common ones:

- Underestimating interest rate risk: With variable loans common in Australia, even a 1% rate increase can add thousands in annual costs.

- Ignoring vacancy periods: Allow at least a four-week vacancy buffer each year.

- Overlooking strata or levy costs: Apartment levies and special fees can rise significantly over time.

- Failing to budget for maintenance: Older properties can require more frequent repairs, which can quickly eat into profits.

- Not matching strategy to cash flow: If your strategy focuses on growth, you may accept some negative cash flow. If you need income, focus on yield.

Common questions investors ask:

- What rent do I need for neutral cash flow? Divide total annual costs by yield expectations.

- Can I claim these costs on tax? In most cases, yes. Many holding costs are deductible if your property produces rental income, but always confirm with a qualified tax adviser or accountant.

- What if interest rates rise or costs increase? Stress-test your model using conservative assumptions to ensure you can still cover costs.

Strategies to Optimise and Reduce Holding Costs

Once you understand your holding costs, the next step is optimisation. Here are a few strategies to improve cash flow:

- Negotiate your interest rate – A small reduction can significantly improve net returns.

- Use a proactive property manager – Reduces vacancies and keeps maintenance expenses under control.

- Buy properties with lower ongoing fees – Freestanding homes often have fewer levies than strata properties.

- Budget proactively for maintenance – Setting aside a yearly sinking fund helps smooth out repair spikes.

- Choose the right location – Higher rental yields in regional or affordable suburbs can provide stronger cash flow stability.

- Regularly update your calculator – Review your property’s numbers every six months or when interest rates change.

Small improvements across these areas can move a property from negative to positive cash flow and improve your investment returns.

Real-World Example

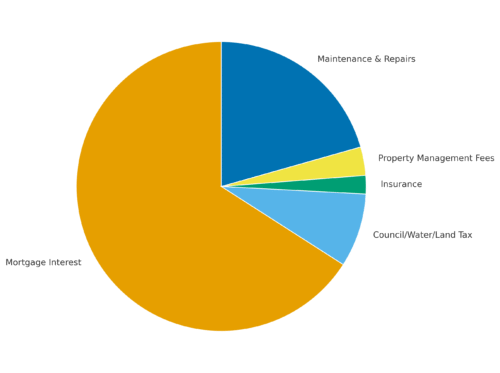

Let’s walk through an example using a $600,000 investment property:

- Weekly rent: $550

- Vacancy: 4 weeks per year → annual rent received $26,400

- Holding costs:

- Interest ($480,000 loan at 8%): $38,400

- Council/water/land tax: $4,800

- Insurance: $1,200

- Property management (7%): $1,848

- Maintenance (2% of value): $12,000

Total holding costs: $58,248

Net cash flow: $26,400 – $58,248 = –$31,848 per year

This example shows how critical it is to evaluate holding costs before purchase. If capital growth is 5–6% annually, the return might still be viable, but the investor must plan for the shortfall. Use a calculator tool or spreadsheet to test your assumptions and make informed choices.

Conclusion

Understanding investment property holding costs is essential to making smart real estate decisions. By using this quick five-minute cash flow method, you’ll gain a clear picture of your true costs and profitability. The more accurately you forecast your numbers, the more confidently you can expand your portfolio.

Ready to take the next step? Contact our team for a personalised review of your investment property’s holding costs.

Disclaimer: This article is for general information only and does not constitute financial or tax advice. Always consult a qualified professional before making investment decisions.

—————————————————————————————————————————–

External Links: