Capital Gains Tax (CGT) is often discussed as a one-time cost that arises only when a property is sold. However, its influence on long-term property wealth runs much deeper. CGT shapes investor behaviour, affects holding periods, influences portfolio structuring, and ultimately determines how much accumulated growth is retained after decades of ownership.

While public discussion sometimes portrays CGT as a major threat to property wealth, long-term evidence suggests the reality is more nuanced. To understand its true impact, it is necessary to examine how growth compounds over time, how the CGT discount functions, and how macroeconomic drivers interact with tax settings.

This article explores CGT from a structural wealth perspective, using independent and policy-based sources to support each section.

The Legislative Framework Behind CGT

Capital Gains Tax is embedded in Australia’s income tax law under the Income Tax Assessment Act 1997. The full legislative provisions can be accessed through the Federal Register of Legislation, which publishes the consolidated law governing CGT events and calculation methods.

Under this framework, CGT applies when a “CGT event” occurs, most commonly upon signing a contract for the sale of property. The capital gain is calculated as the difference between the capital proceeds and the asset’s cost base.

Although the tax is assessed in the year of disposal, its influence extends across the entire ownership period because it affects investment planning decisions from the outset.

The 50% Discount and Long-Term Holding Incentives

One of the most influential components of Australia’s CGT regime is the general discount method introduced in 1999. Individuals and trusts who hold an asset for more than 12 months may reduce their capital gain by 50 per cent before applying their marginal tax rate.

The policy rationale behind this reform was examined in detail by the Australian Treasury in its Review of Business Taxation papers, accessible through the Treasury publications archive.

The introduction of the discount replaced the former indexation system and was designed to encourage long-term investment rather than short-term speculation. From a wealth perspective, this structural incentive supports accumulation strategies. Investors who retain property over longer horizons effectively face a lower average tax rate on real gains.

Over 15 or 20 years, this discounted treatment materially improves after-tax outcomes compared to a full marginal rate on total gains.

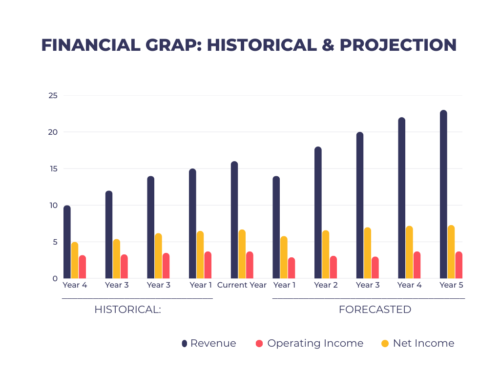

Graph: Steady Historical Performance with Accelerating Growth Ahead

This financial graph illustrates consistent growth in revenue, operating income, and net income across historical years, followed by stronger projected increases in the forecast period. While historical performance reflects stable and gradual expansion, the projected figures indicate improved profitability and upward momentum, suggesting enhanced operational efficiency and sustained financial growth moving forward.

Long-Term Property Growth: The Compounding Effect

Property wealth is fundamentally driven by compounded capital growth. Long-term housing price trends are primarily influenced by population growth, income growth, supply constraints, and interest rates.

Over extended periods, property values have demonstrated sustained upward movement despite cyclical volatility. When growth compounds annually, the bulk of wealth accumulation occurs before CGT is ever triggered.

For example, a property purchased for $600,000 that grows at an average annual rate of 4.5 per cent for 20 years reaches approximately $1.44 million. The capital gain exceeds $840,000. Even after applying CGT at a discounted rate, the majority of accumulated wealth remains intact.

This illustrates that CGT affects the final distribution of wealth, but compounding growth is the primary driver of its creation.

Inflation and Real vs Nominal Gains

A common concern is that CGT applies to nominal gains rather than inflation-adjusted gains. Prior to 1999, Australia allowed cost base indexation. Inflation contributes to nominal price increases over long holding periods. However, the 50 per cent discount partially compensates for inflationary effects by reducing the taxable portion of the gain.

For long-term investors, the interaction between inflation, growth, and discount eligibility typically results in a moderate effective tax rate relative to total appreciation.

Frequently Asked Questions (FAQ)

1. Does CGT significantly reduce long-term property wealth?

CGT reduces final proceeds at sale, but compounded growth over decades generally outweighs the tax burden, particularly with the 50 per cent discount.

2. Is CGT payable annually?

No. CGT is triggered only upon a CGT event, most commonly when the property is sold.

3. Does holding property longer improve after-tax outcomes?

Yes. Holding beyond 12 months qualifies individuals and trusts for the 50 per cent discount, lowering the effective tax rate.

4. Does inflation make CGT unfair?

Inflation contributes to nominal gains, but the discount system partially offsets this effect.

5. Is CGT the main risk to long-term wealth?

Research suggests that interest rates, housing supply, and economic growth have a greater impact on long-term property performance than CGT alone.

6. Can structuring ownership improve CGT outcomes?

Yes. Ownership structure, timing, and retirement planning strategies influence effective CGT outcomes and should be assessed professionally.

EXTERNAL LINKS:

- Quick guide to Capital Gains Tax (CGT)

- An empirical investigation of whether Australian capital gains tax reforms influence individual investor behaviour

- Why Compound Growth is the Real Estate Investor’s Secret Weapon

- Nominal vs. Real Return: How Inflation Affects Investments