Capital Gains Tax (CGT) is often viewed as a transactional issue, something calculated at the point of sale and paid at the end of the financial year. In reality, CGT plays a structural role in shaping investment strategy, particularly when it comes to holding periods.

In property investment, timing the market is often debated. However, history consistently demonstrates that time in the market tends to outweigh attempts to precisely time entry and exit. The interaction between CGT rules and long-term holding periods reinforces this principle.

This article explores how CGT works alongside compounding growth, why the 12-month rule is more significant than many realise, and why extended holding periods continue to support long-term property wealth.

The Legislative Timing of CGT Events

A CGT event typically occurs when a contract for sale is entered into, not at settlement. This distinction influences the financial year in which the gain is assessed and creates planning considerations around disposal timing.

Because the tax is triggered at contract date, investors must evaluate exit decisions strategically rather than reactively. Although CGT is applied only once at disposal, its presence influences investment decisions from acquisition through to sale.

The legal structure does not merely tax profit; it shapes holding behaviour.

The 12-Month Holding Rule and the 50% Discount

Australia’s CGT framework provides a 50% discount for individuals and trusts that hold assets for more than 12 months. This rule fundamentally alters the effective tax rate on long-term capital gains.

A $300,000 capital gain held beyond 12 months results in only $150,000 being included in assessable income. At a marginal tax rate of 37 per cent, the tax payable becomes $55,500 instead of $111,000.

This single provision creates a structural incentive for patience. The tax system directly rewards longer holding periods and discourages rapid turnover.

The implication is clear: time is not merely a growth factor, it is a tax advantage.

Short-Term Selling and Market Volatility

Short-term property transactions carry two structural disadvantages. The first is the loss of the CGT discount. The second is exposure to cyclical volatility driven by interest rates, credit conditions, and macroeconomic shifts.

Property markets move in cycles influenced by broader economic forces. Short-term speculation increases the risk of selling during weaker phases while simultaneously increasing tax exposure.

Extended holding periods reduce the relative importance of short-term fluctuations and allow broader structural growth drivers to play out.

Compounding Growth and Long-Term Wealth

Property wealth is primarily built through compounding appreciation. Growth accumulates annually, whereas CGT is applied once at exit.

Consider a property purchased for $700,000 growing at 4.5 per cent annually.

After 5 years, the value approximates $872,000.

After 15 years, the value approaches $1.35 million.

The longer holding period dramatically increases total gain before tax is applied. While CGT reduces final proceeds, it does not affect the compounding process during ownership.

This asymmetry is critical. Growth compounds every year. Tax does not.

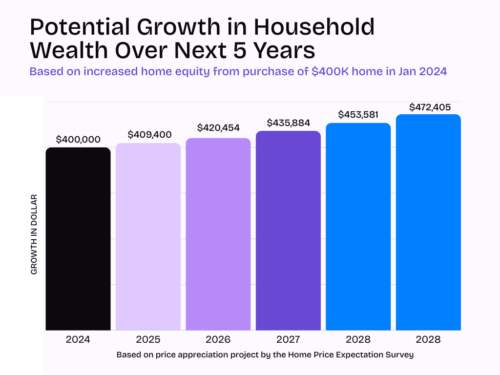

Graph: Holding Period Impact on Net Wealth After CGT

The chart shows how a $400,000 home purchased in 2024 could grow to approximately $472,405 over five years, demonstrating how steady price appreciation can steadily build household equity and long-term wealth.

Table: Holding Period Comparison

|

Item |

5 Years |

15 Years |

|

Purchase Price |

$700,000 | $700,000 |

|

Property Value |

$872,000 |

$1,350,000 |

|

Capital Gain |

$172,000 |

$650,000 |

|

Discounted Gain (50%) |

$86,000 |

$325,000 |

|

Tax at 37% |

$31,820 |

$120,250 |

|

Net After-Tax Proceeds |

$840,180 | $1,229,750 |

The comparison demonstrates how extended timeframes magnify wealth creation despite taxation at exit.

Behavioural Incentives in the Tax System

Tax design influences investor behaviour. A discounted capital gain for assets held longer than 12 months discourages frequent trading and promotes longer-term capital allocation.

Longer holding periods reduce transaction costs, smooth exposure to market cycles, and lower effective taxation relative to total gain. Investors who frequently enter and exit positions face higher frictional costs and greater exposure to timing risk.

The structure of CGT reinforces disciplined, long-term participation rather than speculative activity.

Time vs Timing

Timing attempts to capture precise market peaks. Time allows growth to accumulate through multiple cycles.

CGT does not compound annually. Property appreciation does. The longer the asset is held, the more disproportionate the impact of compounding becomes relative to the final tax payable.

Time in the market does not eliminate risk, but it reduces reliance on perfect forecasting.

Frequently Asked Questions (FAQ)

1. Why does the 12-month rule matter so much?

It halves the taxable capital gain for eligible investors, significantly lowering the effective tax rate.

2. Is selling before 12 months financially inefficient?

In many cases, yes. The full gain is assessable without discount, increasing tax exposure.

3. Does a longer holding period always mean higher returns?

Not automatically, but extended timeframes generally allow compounding growth to outweigh short-term volatility.

4. Does CGT reduce the benefit of long-term growth?

It reduces final proceeds, but it does not affect annual capital appreciation during ownership.

5. Should tax considerations alone determine selling decisions?

No. Broader financial objectives, liquidity needs, and portfolio strategy should also be considered.

6. Is “time in the market” guaranteed to outperform?

No investment outcome is guaranteed, but long-term holding reduces reliance on precise market timing.

Conclusion

Capital Gains Tax and holding periods are structurally linked. The 12-month discount rule rewards patience, while compounding growth amplifies wealth over extended timeframes.

Although CGT reduces proceeds at exit, it does not erode the fundamental mechanism of property wealth creation: sustained growth across economic cycles.

For long-term investors, time remains a strategic asset not only because markets grow, but because the tax system itself is designed to favour those who stay invested.

EXTERNAL LINKS:

- Identify the timing of a CGT event

- Capital Gains Tax Rules in Australia: A CGT Guide for Individuals and Investors and How to Minimise It

- Understanding the Capital Gains Tax (CGT) Discount in Australia I Trinity Accounting Practice

- Capital Gains Tax Discount: The Economics Behind the Debate

- https://www.capitalgroup.com/individual/planning/investing-fundamentals/time-not-timing-is-what-matters.html