If you’ve ever thought about buying property in your SMSF, you’re not alone. Many Australians see property as a way to grow their retirement savings, and SMSFs give trustees the flexibility to invest directly in real estate. But unlike buying in your personal name, SMSF property investments come with strict rules, borrowing limits, and compliance hurdles.

The Australian Taxation Office (ATO) makes it clear that any SMSF property purchase must satisfy the sole purpose test. That means the investment is strictly to provide retirement benefits, not personal enjoyment. In this guide, we’ll break down the rules, the borrowing process, the most common questions, costs you’ll need to budget for, and a step-by-step checklist to help you decide if this strategy is right for you.

SMSF Property Rules You Must Know

Buying property in your SMSF can be powerful, but only if you play by the rules. – No personal use: You or your family cannot live in or use the property, even briefly. The ATO is very clear this would breach the sole purpose test. – Related-party restrictions: Generally, your SMSF cannot buy residential property from a related party. The main exception is business real property, which can be purchased or leased back to your business provided it’s done on commercial terms. – Annual valuation: Every year, trustees must value the property at market value for reporting and audit purposes.

Borrowing & Finance: How SMSF Loans Work

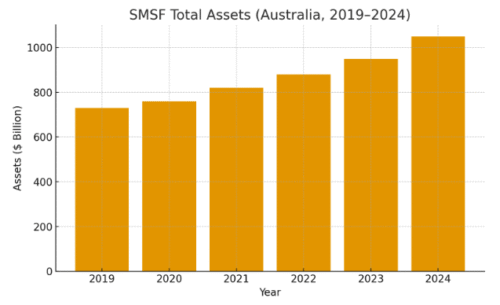

Most SMSFs don’t have enough cash to buy a property outright, which is why limited recourse borrowing arrangements (LRBAs) exist. Under an LRBA, the loan is secured only against the property, the lender cannot touch other SMSF assets if things go wrong. – Deposits & lending terms: Lenders typically require 20–30% deposit and may ask for personal guarantees. Unlike standard property loans, SMSF loans have stricter features; no redraws, limited flexibility, and higher rates. – ATO safe harbour rules: If you borrow from a related party, you must comply with the ATO’s “safe harbour” interest rates and terms. This ensures the deal is at arm’s length and avoids tax penalties. – Sector size: According to APRA, SMSFs now hold over $1 trillion in assets with property representing a large and growing portion.

Common Questions & Misconceptions

“Can I live in the property?”

No. Residential property owned by an SMSF cannot be used by members or relatives. Even short-term stays breach the law (ATO guidance).

“Can my business lease it?”

Yes, but only if it’s business real property and leased at market rates. Many small business owners use their SMSF to buy their office or warehouse, then pay rent to their fund (ATO – business real property rules).

“What happens if I get it wrong?”

Non-compliance can lead to tax penalties, loss of concessional tax treatment, or even the fund being made non-complying. The ATO has powers to fine trustees personally.

Costs, Timelines & Risks

Buying property in your SMSF is more complex, and more expensive, than a regular purchase. Costs to budget for include: – SMSF setup and ongoing annual audit/accounting fees. – Stamp duty and legal fees. – Lender setup costs and higher SMSF loan interest rates. – Ongoing property management, maintenance, and insurance. Timeframes are also longer, as an LRBA requires an additional bare trust structure. From start to finish, expect 3–6 months to complete an SMSF property purchase (MoneySmart). Risks? If the property is vacant or underperforms, your SMSF still has to meet loan repayments. Unlike personal property, you can’t just dip into other savings accounts.

Practical Checklist & Next Steps

- Does your SMSF’s investment strategy allow for direct property?

- Do you have enough funds (and time) to manage costs and risks?

- Have you spoken with a licensed SMSF adviser or accountant?

- Have you compared specialist SMSF loan products?

- Do you have a solicitor to draft the LRBA and bare trust documents?

Conclusion

Buying property in your SMSF can be a powerful wealth-building strategy if done properly. With the right setup, it can diversify your fund, generate rental income, and help you plan for retirement. But it comes with complexity, strict rules, and significant risks. If you’re considering this path, start by reviewing your fund’s investment strategy, speaking with a licensed SMSF adviser, and comparing specialist SMSF lenders. ■ Ready to explore whether SMSF property investment is right for you? Book a free consultation with our SMSF property specialist today.

(General advice only: This content is based on ATO and MoneySmart guidance and is not personal financial advice. Always consult a licensed professional before acting.)

—————————————————————————————————————————–

External Links:

- ATO – LRBA / borrowing restrictions.

- MoneySmart — SMSFs and property (consumer-facing rules).

- APRA / ATO SMSF statistics (use for graphs: SMSF asset totals & trends)

- SMSF Association LRBA guide (practical structuring).