The cost of waiting to invest is one of the most overlooked risks for new investors. Many people assume that delaying their first investment by a few months or even years has little consequence. The truth is quite the opposite. In this article we will examine how postponing your first investment can cost you real money, potentially hundreds of dollars a month in lost opportunity, and provide a clear plan for action. Our thesis: The earlier you invest, the more you benefit from compounding and avoiding the hidden cost of delay, and every month you wait eats into your future wealth potential.

Why delaying your first investment matters

When you delay your first investment you aren’t just waiting, you are giving up the time your money could have spent in the growing market. This is more than a hypothetical: financial advisers often call time the “secret ingredient” in wealth-building. The key concepts here include:

- Compounding interest: returns generate returns; the earlier you start, the more “returns on returns” you get.

- Opportunity cost: money that could be invested today is sitting idle or earning low interest (or worse, being eroded by inflation).

- Momentum and habit: starting early means you build a good habit of investing and see the benefits sooner. Delaying often means you need to invest much more later to catch up.

For example, if you were to start investing $200 a month today, versus waiting one year to start the same amount, the difference in wealth decades later becomes significant. While you might rationalise “I’ll wait until I know more” or “I’ll wait until I earn more”, each month you postpone adds a cost. That “delay first investment cost” mounts silently.

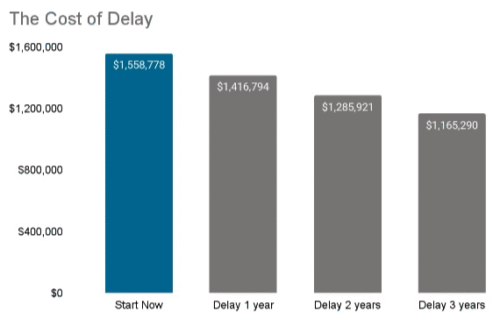

The numbers that show the cost of waiting

Let’s look at some real-world numbers to illustrate “how much does delaying investing cost per month”. One recent scenario from a financial analytics provider shows: delaying investing by just one year with a 8.49 % annual return over a 30-year horizon could cost more than US$320,000. Similarly, another study shows that delaying your systematic contributions by two years could reduce your long-term wealth by ~20%.

To break this down: suppose you plan to invest $250 per month, starting now, at an assumed 7% annual return. If you delay that investment by 12 months, you lose 12 months of that $250 + 7% growth + subsequent compounding. That might amount to the equivalent of ~$3,000–$4,000 (or more) of lost value over decades. Divide that by, say, a 30-year horizon and it essentially means losing the “income-generating potential” of maybe $20-30 per month (or more) depending on your portfolio size.

In Australia, given the effect of inflation and modest return assumptions, the “cost per month” figure of waiting can realistically reach hundreds per month (in lost future income streams) for someone starting later rather than earlier. The important takeaway is: each month you delay is not “just one month off” – it multiplies over time.

Source: Morningstar

Common concerns and questions about starting late

Many prospective investors ask: “What happens if I start investing late?”, “Do I need a large lump sum to start?”, or “Isn’t the market too volatile to invest now?” Let’s address these common concerns:

Concern 1: I don’t have enough money to invest now.

Starting small is fine. What matters is time and consistency more than large initial amounts. Even modest monthly amounts work far better when begun early.

Concern 2: The market looks risky / busy, maybe I’ll wait for the right time.

Trying to time the market often results in delays and lost opportunity. History shows that staying invested tends to outperform waiting for “perfect” timing.

Concern 3: I’m already older / behind. Is it too late?

It’s never “too late” to start, but the cost of waiting is greater when you have fewer years for compounding. For example, someone starting at age 45 rather than 35 may need to invest far more per month to reach the same goal.

Concern 4: What about inflation and fees?

Money sitting in a low-interest savings account is being eaten away by inflation. Investing earlier gives you a higher chance to outpace inflation and fees.

All these show that while it’s natural to have concerns, the bigger risk often is delay and not doing anything.

Strategies to mitigate the cost and start smart

(To provide additional value)

If you’ve realised the cost of waiting is real, here are practical steps to reduce it and get started:

- Automate your investment contributions: set up a monthly direct debit or auto-transfer so you “pay yourself first”.

- Start small and increase gradually: you don’t need a six-figure lump sum. Begin with what you can afford and increase as income grows.

- Use low-cost diversified vehicles: consider index funds or ETFs with low fees; fees erode compounding over time.

- Set a clear timeline and goals: even a rough target helps you stay motivated and track progress.

- Consider employer-sponsored contributions or matching (if applicable): missing these is an additional hidden cost of delay.

- Review regularly and stay consistent: avoid jumping in and out; time in the market tends to outperform timing the market.

These steps help turn the “first investment starting later impact” into a practical action plan.

Conclusion

In summary, the cost of waiting to invest is real, measurable and growing with each month that passes. By delaying your first investment you incur hidden costs: less time for compounding, greater monthly contributions needed later, and a smaller future income stream. The good news is you don’t need perfection to start. Even modest amounts invested regularly can make a significant difference, especially when you start now.

Don’t wait for “the perfect time.” Make this week the moment you take action. Set up a call with us to discuss your goals, explore your investment options, and start building a strategy that works for your future. The best time to invest was yesterday, the next best time is today.

——————————————————————————————————————————-

External links (authoritative sources):

- The price of waiting: Revealing the hidden costs of delayed investing

- The cost of delayed investment

- The Power of Starting Early: Why Delaying Investment Costs You More Than You Think

- Early Earl, Delayed Dennis, and Late Larry: Why Investing early is so important!

- The Hidden Costs of Delaying Your Investments: Why Time Matters More Than Money