Property has long been one of the most popular investment choices inside a Self-Managed Super Fund (SMSF). The appeal is understandable. Property is tangible, familiar to many investors, and often associated with long-term capital growth and rental income, all within the tax-advantaged environment of superannuation.

However, SMSF property is not a universal solution. In certain circumstances, it can increase financial risk, restrict flexibility, and materially weaken retirement outcomes if it no longer aligns with the fund’s balance, cash flow, or investment timeframe. As economic conditions, interest rates, and personal circumstances change, trustees must be prepared to reassess whether holding property inside an SMSF still makes strategic sense.

For a full overview of SMSF investment strategies, visit our SMSF Playbook.

Why SMSF Property Is Often Overestimated

Property held inside an SMSF is subject to stricter rules than property owned personally, particularly in relation to borrowing, liquidity, and related-party use. These constraints are frequently underestimated by trustees, especially first-time SMSF investors.

Unlike property held outside superannuation, SMSF property cannot be lived in or used by fund members or related parties, even temporarily. Transactions must be conducted strictly at arm’s length, and any breach can result in significant tax penalties or compliance action by the Australian Taxation Office (ATO). In addition, property is inherently illiquid, which can create challenges when an SMSF needs to meet expenses, loan repayments, or pension obligations.

Where property is purchased using a Limited Recourse Borrowing Arrangement (LRBA), these challenges are often amplified. SMSF loans typically carry higher interest rates, stricter lending terms, and limited refinancing options compared to standard residential mortgages, increasing the financial pressure on the fund over time.

When SMSF Property Stops Making Sense

1. Your SMSF Balance Is Too Small

SMSFs with lower balances face significantly higher concentration risk when investing in a single, large asset such as property. Industry commentary generally suggests that SMSF property becomes more viable once fund balances exceed approximately $500,000 to $600,000, allowing sufficient capacity to absorb costs, maintain cash buffers, and diversify other investments.

When fund balances fall below this level, a single property can dominate the portfolio, leaving little room to manage unexpected expenses, vacancies, or interest rate increases. This lack of diversification can materially increase volatility and reduce the fund’s ability to respond to changing market conditions.

2. Cash Flow Is Tight or Negative

Property ownership involves ongoing expenses that extend well beyond loan repayments. Maintenance, insurance, property management fees, land tax, and compliance costs can materially erode net returns. Major banks and research houses, including Morgan Stanley, have highlighted that investors often underestimate the true holding costs of property, particularly during periods of higher interest rates.

Within an SMSF, sustained negative cash flow can force trustees to inject additional contributions simply to keep the property viable. This may place pressure on contribution caps and increase the risk of compliance breaches if the fund is unable to meet its obligations.

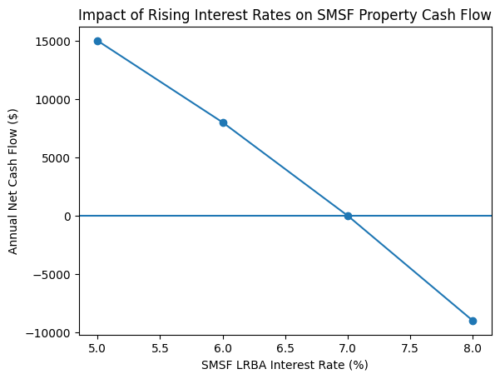

3. Rising Interest Rates Are Hurting Returns

SMSF loans generally attract higher interest rates than owner-occupied or standard investment loans and offer limited flexibility when refinancing. The ATO publishes safe harbour benchmark interest rates for LRBAs, but even within these parameters, rising rates can significantly reduce or completely eliminate net cash flow.

The graph below illustrates how increasing LRBA interest rates can rapidly move an SMSF property investment from positive cash flow into a neutral or negative position. This dynamic is particularly relevant in the current interest rate environment, where higher borrowing costs are expected to persist longer than initially anticipated

4. Lack of Diversification

Diversification and liquidity are core principles of prudent SMSF investment strategy. Holding a single property in one location and asset class creates concentration risk that may not align with a trustee’s stated investment objectives or risk tolerance.

ATO guidance requires trustees to demonstrate that their investment decisions consider diversification, liquidity, and the fund’s ability to meet liabilities as they fall due. A property-heavy SMSF may struggle to satisfy these requirements, particularly if market conditions deteriorate or the fund’s circumstances change.

5. Approaching Retirement or Pension Phase

As SMSFs transition into pension phase, liquidity becomes increasingly important. Minimum pension payment requirements must be met each year, and these payments must be made in cash. Property-heavy SMSFs often face difficulty meeting these obligations without selling assets or drawing heavily on limited cash reserves.

In some cases, trustees may be forced to sell property under unfavourable market conditions simply to meet pension requirements, potentially locking in suboptimal outcomes.

SMSF Property vs Alternative Strategies

|

Strategy |

Liquidity | Diversification | Cash Flow Flexibility | Ongoing Costs |

Suitable for Smaller SMSFs |

|

SMSF Property |

Very Low | Poor | Rigid | High |

No |

|

ETFs |

High |

Excellent |

Flexible | Low |

Yes |

|

Managed Funds |

High | High | Moderate | Medium | Yes |

| Cash & Term Deposits | Very High | Low | Very High | Very Low |

Yes |

What to do instead

For many trustees, a diversified ETF portfolio can provide broad market exposure, lower ongoing costs, and significantly higher liquidity than direct property. Managed funds and model portfolios may also offer professional oversight and alignment with retirement timelines, helping reduce concentration risk while maintaining growth potential.

For SMSFs that already hold property, a hybrid approach may be appropriate. This could involve gradually rebalancing into more liquid assets, reviewing LRBA sustainability, or planning a strategic sale well before pension phase to avoid forced decisions later. Professional advice is essential when making these changes to ensure compliance with SMSF regulations and alignment with long-term objectives.

Trustees considering their next steps may benefit from reviewing their options with an experienced adviser through a structured consultation.

Book a consultation with our SMSF specialists to review your property strategy

Frequently Asked Questions (FAQ)

- When should I reconsider SMSF property? If your fund has low liquidity, rising loan costs, or is nearing retirement, a review is essential.

- Is SMSF property always a bad idea? No. It can suit large, well-funded SMSFs with long-term horizons and strong cash flow.

- Are ETFs safer than property? ETFs generally offer better diversification and liquidity, though all investments carry risk.

- Can I sell an SMSF property before retirement? Yes, provided the transaction is at market value and complies with SMSF rules.

SMSF property is not a one-size-fits-all solution. As interest rates, regulations, and personal circumstances change, strategies must evolve.

The most successful SMSF trustees regularly reassess whether their investments still align with their retirement goals.

External Links:

- SMSFs and Property: Mixing property and your self-managed super

- Shares vs Property Investment in Australia: The Hidden Costs Most People Ignore

- What Are the New ATO Safe Harbour Rates for 2025–26

- Laying the Foundation for Your SMSF Investment Strategy

- Liquidity & Pension Strategy for Property-Heavy SMSFs

- Comparative Review: Investing in a SMSF to Buy Property Versus Buying a Portfolio of ETFs