Introduction

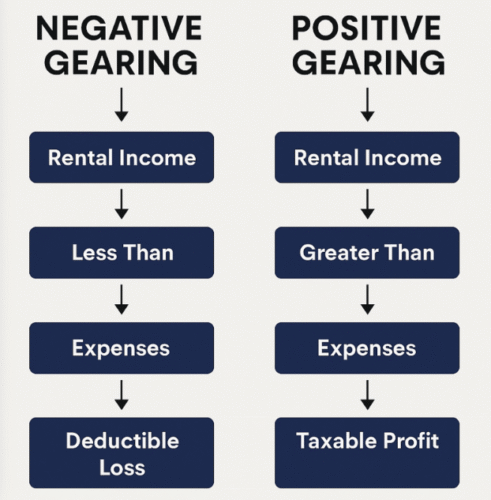

Negative gearing explained Australia is vital for anyone weighing property investment strategies. In simple terms, negative gearing means your rental income is less than your expenses, creating a net loss. This loss can be deducted from your taxable income, making it attractive for high-income investors seeking tax offsets.

However, there’s more to it than just tax breaks. Understanding how this works, its long-term implications, and how it compares to other strategies like positive gearing is key to deciding if it’s the right fit for your financial goals. In this guide, we’ll unpack how negative gearing works in Australia, the potential tax benefits, associated risks, and whether this investment tactic is worth it for your situation.

Section 1 – How Negative Gearing Works

At its core, negative gearing involves borrowing to invest in a property where the annual rental income is less than the total annual expenses. These expenses typically include mortgage interest, maintenance, insurance, property management fees, and depreciation.

The resulting loss can be deducted from your overall taxable income, reducing your annual tax bill. For example, if your property generates $25,000 in rent annually but costs $35,000 in expenses, you can deduct the $10,000 loss from your taxable income.

This is in contrast to positive gearing, where the rental income exceeds expenses, resulting in net income-but this income is taxed. Some investors use a hybrid strategy, starting with negative gearing and transitioning to positive as rents increase over time.

Section 2 – Tax Benefits & Wealth Gains

The primary draw of negative gearing is the potential tax benefit. In Australia, investors in higher tax brackets may significantly reduce their taxable income, especially if they own multiple negatively geared properties. According to the Australian Treasury, high-income earners capture a majority of the benefit-with 30% of top earners claiming over 60% of all negative gearing deductions.

This tax treatment helps smooth cash flow while investors wait for long-term capital growth. For instance, if a property appreciates 6-8% annually, the increase in equity over a 10-year horizon can vastly outweigh the short-term losses.

Real-life case studies, like the ‘Bob and Mary’ scenario from Hudson Financial Planning, show that even a modestly geared property can add hundreds of thousands in net worth when held over a full property cycle.

Section 3 – Risks, Drawbacks & FAQs

Despite the upside, negative gearing has real risks. The most immediate concern is ‘cash flow stress‘. You must be able to cover the shortfall out of pocket each year, especially if interest rates rise. In 2023-2024, with rates around 4.35%, many investors found themselves strained by increased loan servicing costs.

Second, property values are not guaranteed to rise. Economic downturns, over-supply in certain markets, or changing government policies can stall or reverse capital gains.

Common FAQs:

- Is negative gearing only for wealthy people? No, but the benefits are greater for those in higher tax brackets.

- Does it harm housing affordability? Some argue it inflates demand and prices, but research suggests limited impact if properly managed.

- Can it be used with other tax strategies? Yes, many investors combine it with depreciation claims and capital gains concessions.

Section 4 – Is Negative Gearing Worth It?

This depends on your financial goals, risk appetite, and time horizon. If you’re in a high tax bracket and investing in a growing market like Brisbane or Adelaide, negative gearing can reduce your tax bill now and boost wealth over time.

However, investors must prepare for:

– Cash reserves to weather short-term losses

– Property market volatility

– Possible policy reforms

Many experts recommend stress-testing your investment plan-run the numbers at 1-2% above current interest rates, and ensure you’re comfortable covering the gap for 5-7 years. If that scenario still fits your goals, negative gearing may be a powerful wealth-building tool.

Conclusion

Negative gearing remains one of the most widely used investment strategies in Australia, but it is not without risks. From tax offsets to long-term growth, it offers clear advantages to those who understand and plan for its potential downsides. If you’re considering this approach, consult with a financial adviser or property strategist to assess your cash flow, tax position, and market entry point. As with any strategy, knowledge and preparation are key.

___________________________________________________________________________

Internal:

- Positive vs Negative Gearing Case Studies

- Managing Cash Flow in Property Investment

- Interest Rate Impact on Rental Yields

- Property Investment for Low-Income Earners

External:

- ATO guide – rental property deductions

- RBA data on interest rate trends

- ABS reports on housing policy and affordability

- The Guardian: costs and benefits of negative gearing