Most SMSF trustees spend years focused on acquisition such as suburb selection, rental yield, LVR, and long-term capital growth. Yet one of the biggest risks is not how you buy, but how you exit.

Many trustees assume they will simply “sell at retirement.” In reality, market cycles, liquidity pressures, tax timing, and compliance obligations often force unplanned decisions.

Many SMSF property investors structure their fund around a long-term holding assumption, yet superannuation law does not guarantee ideal market conditions at retirement. Trustees must consider that retirement dates, health events, legislative changes, and economic cycles rarely align perfectly. Without a documented exit framework, trustees risk making reactive decisions rather than strategic ones. Exit planning is not pessimistic, it is prudent governance under trustee obligations.

Why Exit Strategy Planning Matters

Under the Superannuation Industry (Supervision) Act 1993 (SIS Act), trustees must ensure investments align with the fund’s documented investment strategy and liquidity needs. Failing to plan for exit can create:

- Liquidity shortfalls

- Forced sales during downturns

- Breaches of diversification guidelines

- Pension payment pressure

- Reduced retirement outcomes

The Exit Strategies Trustees Rarely Plan For

1. Selling During Accumulation Phase

Many trustees assume they will hold until the pension phase. However, selling during accumulation may be strategic if:

- Market growth targets are achieved early

- The fund needs diversification

- Interest rates materially affect cash flow

Capital gains tax (CGT) is typically 15% in accumulation, reduced to 10% if held longer than 12 months (after discount).

Selling during accumulation can also allow trustees to rebalance asset allocation back toward shares, fixed income, or cash to reduce concentration risk. Many SMSFs become overly property-heavy over time due to capital growth, which can distort diversification targets outlined in the fund’s investment strategy.

A proactive sale in accumulation may strengthen long-term sustainability, particularly if the property represents more than 50–60% of total fund value.

2. Transitioning to Pension Phase Before Sale

Once a member moves to the pension phase, earnings including capital gains may become tax-free (subject to transfer balance cap limits).

This strategy can significantly alter net outcomes.

However, trustees must carefully model timing. The transfer balance cap limits how much can move into the tax-free pension phase. If the property value exceeds available cap space, only a portion of the gain may receive tax-free treatment.

3. In-Specie Transfer to a Member

In some cases, the property may be transferred out of the SMSF to a member at market value.

Important considerations:

- Stamp duty may apply

- CGT event is triggered

- Valuation must be independent

In-specie transfers are often considered when members wish to retain a high-performing property personally. However, trustees must ensure the transaction is conducted at arm’s length and supported by an independent market valuation to avoid compliance breaches.

This strategy can be beneficial in estate planning scenarios but must be weighed against transaction costs and liquidity consequences for the remaining fund members.

4. Selling Due to Liquidity Pressure

Liquidity risk is often underestimated.

If rental income drops or interest costs rise, trustees may be forced to sell during unfavorable market conditions.

Liquidity stress can arise from multiple sources: prolonged vacancy, rising interest rates under a Limited Recourse Borrowing Arrangement (LRBA), unexpected maintenance expenses, or minimum pension payment requirements.

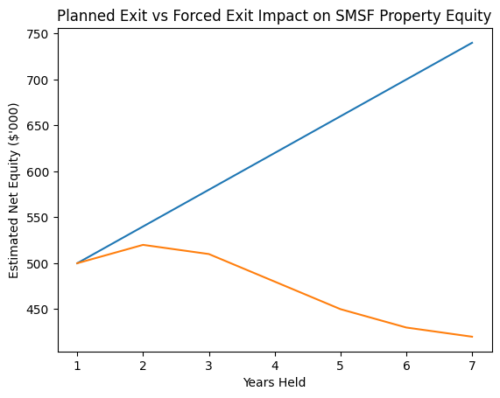

SMSFs holding a single property asset are particularly vulnerable. Without adequate cash buffers, trustees may have no choice but to sell at suboptimal market timing, potentially locking in lower-than-expected retirement outcomes.

Below is a visual comparison of a planned exit versus a forced exit under pressure.

A forced sale during declining equity can permanently reduce retirement capital.

Comparison Table: Exit Pathways

|

Exit Strategy |

When Used | Tax Impact | Liquidity Impact |

Risk Level |

|

Sell in Accumulation |

Growth target met early | Up to 15% CGT (10% discounted) | Improves liquidity |

Moderate |

|

Sell in Pension Phase |

Retirement phase | Potentially 0% CGT | Improves liquidity | Low (if planned) |

|

In-Specie Transfer |

Member wants ownership | CGT + possible stamp duty | Neutral to fund |

Moderate– High |

|

Forced Sale |

Cash flow shortfall | Depends on phase | Emergency relief only |

High |

Compliance Considerations Trustees Overlook

Under guidance from the Australian Securities and Investments Commission (ASIC) and the ATO, trustees must:

- Regularly review their investment strategy

- Consider liquidity and diversification

- Document exit assumptions

- Ensure related-party transactions meet market value requirements

Additionally, trustees must ensure their investment strategy explicitly addresses liquidity, diversification, and the ability to discharge liabilities as they fall due.

A strategy that merely states “long-term capital growth” without addressing exit mechanics may be considered insufficient documentation. Annual reviews should include written commentary on whether exit assumptions remain appropriate.

Advanced Exit Planning Factors

- Member Age Gaps – If one member retires earlier, pension withdrawals may pressure property cash flow.

- Borrowing Structures (LRBA) – Limited Recourse Borrowing Arrangements (LRBAs) restrict flexibility and refinancing options.

- Market Cycle Timing – Property cycles rarely align perfectly with retirement timing.

- Death or Incapacity of a Member – Binding death benefit nominations may require asset sale to pay beneficiaries.

Trustees should also consider legislative risk. Superannuation regulations, transfer balance caps, and borrowing rules may change over time.

An exit strategy built solely on today’s rules may not remain optimal in ten years. Scenario modelling including early retirement, partial disability, market downturn, or regulatory reform strengthens long-term resilience.

Practical Exit Planning Framework

- Define ideal exit year range

- Model tax outcomes in accumulation vs pension phase

- Stress-test rental vacancy and rate rises

- Maintain liquidity buffer (6–12 months expenses minimum)

- Document strategy review annually

Trustees should revisit this framework annually or whenever major life events occur. Documentation of exit planning discussions during trustee meetings strengthens compliance evidence and demonstrates prudent governance. A well-documented exit pathway also improves adviser collaboration and audit clarity.

If you are anxious, consult an SMSF specialist accountant and a licensed adviser immediately. Delaying making decisions usually worsens the situation.

And if you are thinking about buying property through your SMSF or maybe you already have and want a quick sanity check, now’s a good time to get clear on where you stand. TALK TO US and let’s stress test your plan and double-check you’re sticking to ATO rules. You’ll thank yourself down the track.

Frequently Asked Questions (FAQ)

When should an SMSF sell an investment property?

When liquidity requirements, diversification needs, pension transitions, or market conditions justify it not purely based on retirement timing.

Is capital gains tax payable when selling SMSF property?

Yes in the accumulation phase (up to 15%, discounted to 10% if held >12 months). Potentially 0% in the pension phase, subject to transfer balance cap rules.

Can I transfer my SMSF property to myself?

Yes, via in-specie transfer at market value. CGT applies and stamp duty may apply depending on state legislation.

What happens if my SMSF cannot meet pension payments?

Trustees may need to liquidate assets, including property, to meet minimum pension standards under SIS regulations.

Does the ATO require an exit strategy?

The ATO requires trustees to maintain and review an investment strategy that considers liquidity and risk which inherently includes exit planning.

EXTERNAL LINKS:

- SMSF Investment Strategy: The Ultimate Guide Every Trustee Needs

- Guide to limited recourse borrowing arrangements

- Buying Property with your Superannuation

- Prepare an exit plan

- SMSFs and property