For most Australians, property is the biggest thing on their personal balance sheet. In the past, “risk” usually meant vacancy periods, rising interest rates, or maybe too many new apartments in the area. Now, climate risk has quietly joined the list—and it’s not just a theory anymore. New national data shows climate hazards are already changing what homes are worth, how much it costs to insure them, and how banks look at lending.

The government’s first National Climate Risk Assessment lays it out: climate dangers could wipe hundreds of billions off property values if we don’t adapt. That’s not some far-off scenario. The Climate Council and PropTrack say flood risk alone has already knocked over $42 billion off the value of Australian homes. Properties in marked flood zones are selling at obvious discounts.

So, if you own or want to buy an investment property, climate risk isn’t just a footnote on your checklist—it’s front and center.

Climate risk is already shifting the value of Australian real estate

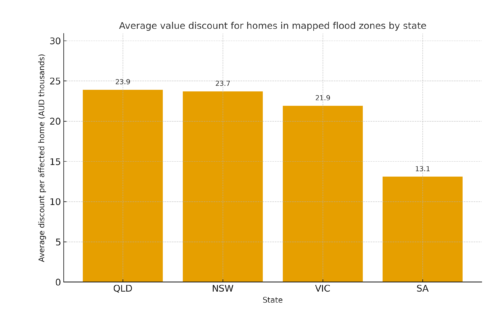

Recent research from Climate Council and PropTrack shows about one in six Australian homes sits in a mapped flood zone. Homes in these areas are typically valued around $75,000 less than similar places outside the risk zone. In some Queensland and New South Wales suburbs, the discount’s even bigger.

Domain’s Perils report shows just how many homes sit in the firing line:

- About 5.6 million homes face bushfire risk—that’s nearly half the country’s housing.

- Over 900,000 homes have some level of flood risk.

- Roughly one in ten homes within 150 meters of the coast risks coastal erosion.

The National Climate Risk Assessment suggests that under high emissions, property value losses by mid-century could reach into the hundreds of billions.

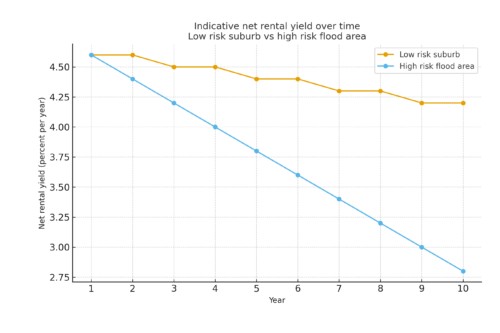

If you’re an investor, the message is pretty clear. The market is now splitting climate resilient homes from those likely to get hit by floods, fire, or coastal damage. This repricing is picking up speed as better data comes in and buyers, insurers, and banks start to act on it.

Floods, fires, coastal erosion: three hazards you need to price in

Flood risk and low-lying suburbs

Flooding has always been Australia’s costliest disaster. Look at Brisbane, Lismore, and other river towns. Whole suburbs went from insurable to “forget it” almost overnight—or insurance got so pricey it barely made sense.

For investors, here’s what that means:

- Higher insurance premiums and excesses eat into your returns.

- It gets harder to find tenants after repeated floods.

- You may have to sell at a discount, or can’t sell at all.

The Property Value Flood Risk report shows these aren’t “what ifs” anymore. It’s already happening, and you can see it in the sales data.

Bushfire exposure in regional and peri-urban belts

Big chunks of regional New South Wales, Victoria, South Australia, and Western Australia are bushfire-prone. Domain says millions of homes sit in these areas, with total exposure in the trillions of dollars.

Insurance in some “tree change” towns has shot up, and councils are getting stricter on what you can build and where you can plant trees. Bushfire risk doesn’t always make a property a bad bet, but you need to price it in. Older studies show buyers sometimes ignore the warning signs—until a big fire hits, and then prices tank.

Coastal erosion and sea level rise

Coastal property used to feel like a safe bet. Not anymore. National Climate Risk Assessment and other research now highlight how much exposure there is along low-lying coastlines. Rising seas and storm surges could threaten hundreds of thousands of homes by mid-century.

Investors are already seeing:

- Higher premiums or new insurance exclusions for storm surge.

- Tougher planning rules and building codes.

- The possibility of government buybacks, not normal sales, down the track.

Some insurers have started limiting cover for storm surge, especially after recent cyclones and east coast storms.

How climate risk hits your cash flow, loans, and property values

Climate risk isn’t just about physical danger. It hits your bottom line in three big ways.

Insurance premiums—and uninsurable homes

Reports from the Climate Council and others talk about the rise of “uninsurable homes.” In some flood or cyclone-prone regions, insurance is hard to get—or it comes with sky-high premiums and excesses. Sometimes, you’re looking at tens of thousands a year just to insure the place.

That extra cost eats straight into your rental income. At some point, the yield just doesn’t stack up, especially if tenants are also facing higher insurance and living costs.

Bank credit policies and valuation haircuts

Lenders are gradually factoring-in climate risks in their credit decision-making process. Brokers and banking industry sources, through their public commentaries, indicate that

- Approval of high-risk location cases is receiving extra scrutiny

- On the other hand, property valuers may look to the application of valuation discounts in the cases of properties situated in areas prone to flooding or those that have been earmarked for forest fires.

- The capital requirements for loan books that are exposed to climate risk may increase over time. This increase can, in turn, work its way into the Interest margins.

For an investor, this can translate into a lesser ability to borrow or lower options for releasing equity, especially if several properties have similar exposures to the climate.

Strata, special levies and rebuild costs

For the risk of climate change in units and townhouses, it may manifest in the following:

- Rising of common insurance premiums

- Special levies for flood mitigation, fire compliance, and coastal protection

- Build costs going up as codes and standards take into account higher climate risks

Most of these money costs often make a surprise visit years after the purchase, thus it is quite easy to underestimate them at the start.

A practical climate risk checklist for Australian property investors

Below is a doable checklist for you to personalize for your own location and lead magnets while being in the sphere of general information.

One, assess the physical hazard

- Look at local government flood maps and bushfire overlays

- Use the Australian Climate Service tools and state environment agencies to view flood, fire, and coastal risk layers

- Don’t rely only on long-term averages, check recent event history as well

Two, understand insurance reality before you buy

- You need to get written quotes for building and landlord cover at the exact location. The quotes should also include flood and fire extensions.

- Inquire about excesses, exclusions, and any special conditions

- Make sure that if tenants are given contents cover, it will be at a reasonable price

Three, review planning controls and reports

- Look through Section thirty-two or equivalent disclosure material thoroughly

- References to past flood or fire events as well as mitigation works can be found in the text

- Local plans may indicate rezoning, buyback, or adaptation programs that you should note

Four, inspect for resilience features

Purchasers are not in a position to remove climate risk from the Australian property market, but they can choose the homes that have features that make them more resilient, for instance,

- Upper floor levels that are above historical flood heights, or homes with split-level designs

- Construction materials that are fire-resistant, defensible spaces, and areas that are fire-service accessible

- Properly serviced drainage, retaining walls, and coastal protection (if applicable)

Such features can facilitate long-term value even in regions that are of higher risk.

Positioning your portfolio for a climate smart future

Most investors would not question the existence of climate change. Instead, the question would be whether the portfolio you currently have will still be viable when risk data becomes more accurate and capital markets change.

Some sensible portfolio-level changes with your financial advisor to think about:

- Rather than assuming that every property you own is equally exposed to climate risks, you should map your current holdings against known climate hazards.

- Try to prevent the concentration of one hazard for instance by not having several properties on the same floodplain or in the same fire corridor

- By new purchases, you can move in a direction that is more beneficial for you in terms of both climate and location measures by focusing on places with good employment and infrastructure.

- Deliberate the contribution of the newer, more energy-efficient, housing stock where the resilience is integrated into the design, particularly for long-term holdings

The National Climate Risk Assessment is quite explicit that climate risk has become systemic. It is a gradual process of every level government, lender, and insurer embedding it in their decisions. Investors who begin to consider it in their pricing today are more likely to safeguard both income and capital during the next decades.

Climate risk Australian property market dynamics are not backbench issues anymore. Floods, fires, and coastal hazards are already reflected in sales data, insurance premiums, and lending settings. The message for investors is thus straightforward.

It is not necessary for you to stay away from every climate-exposed suburb; however, you do need to comprehend the exact dangers, perform realistic calculations for insurance and maintenance, and contemplate how each asset would function if there were frequent extreme events.

Make time to

- Carry out an audit of your present portfolio for climate exposures

- Upgrade your due diligence checklist to be ready for the next purchase

- Qualified professionals can help you greatly in understanding how climate risk interacts with your overall strategy

By doing this work now, you will not only be able to manage the downside risk, but it also can bring to the surface resilient locations and assets that remain attractive as the market adjusts.