Purchasing real estate within a self-managed super fund makes sense. Control, potential long-term growth, and rent flowing into the super. It makes sense that over $100 billion in SMSF funds currently reside in physical locations throughout Australia.

However, trustees fall into the same SMSF property traps each year. Certain traps cause excruciating stress related to cash flow. Others lead to violations of Australian Taxation Office regulations and may even jeopardize the fund’s future.

This article only contains general information. It doesn’t take into account your needs, goals, or financial circumstances. Consult an SMSF specialist and a licensed financial advisor who can thoroughly examine your circumstances before taking any action.

Let us walk through five SMSF property traps that regularly catch Australian investors, plus practical ways to avoid them.

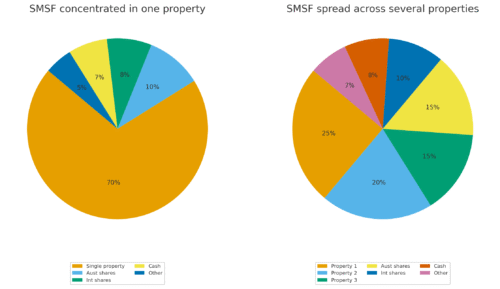

Trap 1: Concentrating your SMSF in a single property

For many trustees, the SMSF property plan seems straightforward. They roll existing super into a new SMSF, borrow through a limited recourse borrowing arrangement, buy one property, and let time and rent work for them.

The issue is concentration. If that single property makes up most of your SMSF balance, you risk a lot in one asset, one tenant, one location, and one sector. If the tenant leaves, repair costs rise, or the local market slows just before your retirement, your entire plan is at risk.

ATO guidelines require trustees to have an investment strategy that considers diversification, risk, liquidity, and the fund’s ability to pay benefits. A single geared property can make it tough to meet those criteria convincingly.

Practical ways to avoid this trap:

- Don’t put your entire super balance into one SMSF property deal.

- Keep enough in liquid assets like cash and diversified funds to cover costs and pension payments.

- Review your investment strategy in writing before and after any property purchase.

Trap 2: Breaching SMSF property and related party rules

Australian law doesn’t mess around. If your SMSF owns a residential property, you or your family can’t live there; it doesn’t matter if you pay full market rent. You also can’t buy the place from a relative in most cases. Everything comes back to one rule: the property has to be there for your retirement, not for family holidays or a place for your kids to crash.

Still, every year, trustees get caught. Someone lets their adult kids stay in the SMSF unit for a few months. Someone else buys a beach house through their fund and sneaks in for a weekend. Others try to shift an old investment property into the SMSF without checking the rules. It happens more than you’d think.

And the risks? They’re serious. Your fund can lose its tax perks, get hit with big penalties, or even become non-complying. The ATO isn’t blind to this stuff—they watch SMSF property deals closely and have plenty of power to crack down.

So how do you avoid trouble?

- Treat your SMSF like it’s a separate person, not just another part of your life.

- If you’re thinking about a deal with a relative, get advice in writing before you do anything.

- And whenever you feel tempted to use the property yourself, stop and check the sole purpose test again. If it doesn’t stack up for retirement, it’s not worth the risk.

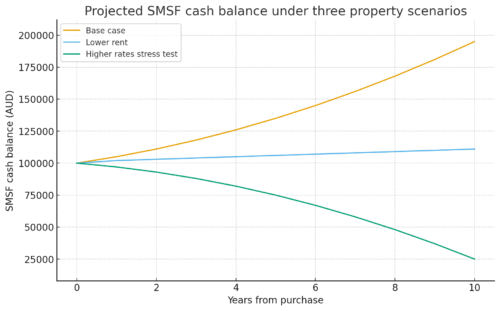

Trap 3 Underestimating SMSF loan and cash flow risk

It is quite common for many SMSF trustees to employ limited recourse borrowing arrangements when purchasing property. Essentially, these loans are subject to tighter regulations, usually higher interest rates, and stricter loan-to-value ratios compared to standard home loans. Moreover, lenders may require the fund to have a substantial amount of liquid assets after the settlement.

The trap is in the assumption that the rent will always be enough to cover the repayments with money left over. The truth is quite often different. Vacancy periods, rising interest rates, maintenance, and insurance costs, as well as higher audit and administration fees, can all lower the cash flow of the SMSF. In case contributions are capped or vary due to changes in employment, the fund will become very limited quickly.

How to practically reduce loan and cash flow risks?

- Test your numbers by including higher interest rates and lower rent in your projections

- Besides the settlement costs, maintain a good cash buffer in the SMSF

- Know the implications if one member ceases to contribute, retires earlier than expected, or draws a pension

Trap 4 Signing contracts in the wrong name or using the wrong structure

To purchase property with a self-managed superannuation fund (SMSF), owners typically use a bare trust or custodianship arrangement which provides ownership of the property to the bare trust, but gives the SMSF the right to benefit from any rents derived from it. It is critical for buyers of property with an SMSF to work with an experienced SMSF Solicitor throughout the entire process because there are strict time limits for completing transactions and, when under such duress, it is common for buyers to sign contracts for the property in their personal capacity or in the name of an entity that is not the trustee of the SMSF or the bare trust.

This situation can lead to a large financial loss. Banks may not allow the transaction to proceed, Stamp Duty may need to be paid twice where contracts have to be re-executed, and in certain situations, it will not be possible to remedy the situation mysmsfproperty.com.au/how-to-buy-property-in-a-smsf in compliance with the SMSF legislation.

You can reduce your exposure to the trap identified above by:

- Engaging a Solicitor with SMSF experience to assist with the contract prior to signing the contract;

- Confirming with your adviser and lender exactly which entity should be shown on the contract and within the Bare Trust Deed; and

- Providing additional time for your financiers and your solicitor to execute the contract and obtain the necessary approvals to complete the purchase through your SMSF.

Trap 5 Treating SMSF property as a set and forget strategy

Property inside super is not a set-it-and-forget-it asset. Trustees must regularly review the investment strategy, insurance, diversification, rent, and expenses. On top of that, the rules continue to change. This includes expectations for documentation, valuation, and limited recourse borrowing rules.

Too many trustees buy properties and then stop paying attention. Rent falls behind, valuations aren’t updated, and changes in member age or pension status don’t get reflected in the strategy. This leaves the fund vulnerable during an ATO review and can result in poor retirement outcomes.

Good practice looks like:

- Annual review of your SMSF investment strategy, including property

- Regular market rent checks and written valuations when needed

- Ongoing contact with your accountant, adviser, and lender about any changes in your circumstances

Frequently asked questions on SMSF property traps

Is SMSF property still worth considering?

Yes, SMSF property might be a good idea for a trustee who is the right person and gets the right advice. The main thing is to understand the rules, risks, and diversification instead of using it as a shortcut to riches.

How much super do I really need before I even think about SMSF property?

Specialist lenders and advisers usually require that the fund balances remain at least between $150,000 and $250,000 after settlement and costs. The right number for you will be determined by your age, contributions, loan size, and other assets. Here, personal advice is indispensable.

Can I fix a mistake after I have already bought?

In some ways. There are possibilities to change the structure, refinance, or even cancel a transaction, but the time frames and costs can be considerable. If you are anxious, consult an SMSF specialist accountant and a licensed adviser immediately. Delaying making decisions usually worsens the situation.

SMSF property traps are out there, but you don’t have to fall into them. Watch out for these five big ones: putting all your eggs in one property basket, breaking the main property or related party rules, overlooking the risks of SMSF loans and cash flow, signing contracts under the wrong structure, and thinking your SMSF property will just take care of itself.

Thinking about buying property through your SMSF? Or maybe you already have and want a quick sanity check? Now’s a good time to get clear on where you stand. TALK TO US and let’s stress test your plan and double-check you’re sticking to ATO rules. You’ll thank yourself down the track.

__________________________________________________________________________

External Links:

- SMSFs and the property boom: rebalancing for a more secure future

- SMSFs and property

- SMSFs and Property Investing: Smart Strategies, Common Mistakes and What to Watch

- SMSF loans

- How to buy Property in a SMSF

- A Guide To Buying Property Through An SMSF

- When SMSF Property Goes Wrong – Real Examples & Consequences